This afternoon Robinhood filed to go public. TechCrunch’s first look at its results can be found here. Now that we’ve done a first dig, we can take the time to dive into the company’s filing more deeply.

Robinhood’s IPO has long been anticipated not only because there are billions of dollars in capital riding on its impending liquidity. But also, because the company became something of a poster child for the savings and investing boom that 2020 saw and the COVID-19 pandemic helped engender.

The consumer trading service’s products became so popular, and enmeshed in popular culture thanks to both the “stonks” movement and the larger GameStop brouhaha, that the company’s public offering carries much more weight than that of a more regular venture-backed entity. Robinhood has fans, haters, and many an observer in Congress.

Regardless of all that, today we are digging into the company’s business, and financial results. So, if you want to better understand how Robinhood makes money, and how profitable or not it really is, this is for you.

We will start with a more in-depth look at growth and profitability, pivot to learning about the company’s revenue makeup, discuss a risk factor or two, and close on its decision to offer some of its own shares to its users. Let’s go!

Inside Robinhood’s growth engineBefore we get into the how of Robinhood’s growth, let’s discuss its how big the company has become.

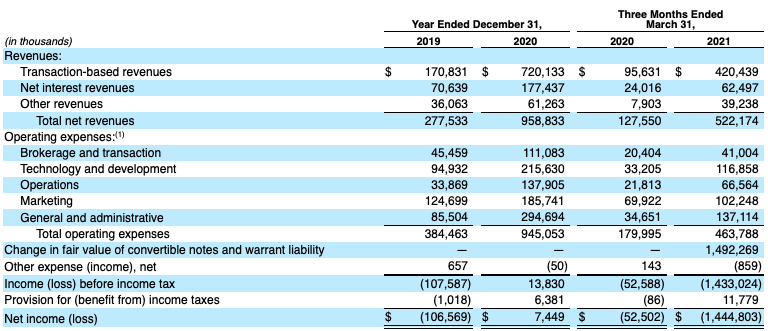

The fintech unicorn’s revenue grew from $277.5 million in 2019 to $958.8 million in 2020, which works out to growth of around 245%. Robinhood expanded even more quickly in the first quarter of 2021, scaling from year-ago revenue of $127.6 million to $522.2 million, a gain of around 309%.

Those are numbers that we frankly do not see often amongst companies going public; 300% growth is a pre-Series A metric, usually.

Returning to our point about how famous the company has become, we can see in its financial performance — tied as it is to user activity, which we’ll get to shortly — why Robinhood’s IPO will prove noisy. It’s going public because of rapidly-scaling usage form consumers, usage that in turn helped the company’s size flat explode in the last year.

Now let’s talk profitability. Here’s Robinhood’s main income statement, which we’ll both need to discuss the company’s red and black ink:

In 2019 Robinhood’s net losses were not small, with the firm posting a $106.6 million deficit, inclusive of tax costs. However, the next year’s growth turned that all around for Robinhood, with the company managing to end the year just in the black — in percent of revenue terms — with net income of $7.4 million.

The company’s 2019 net loss, however, was not spread out amongst its quarters in a uniform fashion; net losses ramped from around $12 million in both Q1 and Q2 2019 to $38.4 million and $44.6 million in Q3 and Q4 of the year, respectively.