Zoom trades at $86.21 and has moved in lockstep with the market. Its shares have returned 15.2% over the last six months while the S&P 500 has gained 11.1%.

Is there a buying opportunity in Zoom, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Do We Think Zoom Will Underperform?

We don't have much confidence in Zoom. Here are three reasons you should be careful with ZM and a stock we'd rather own.

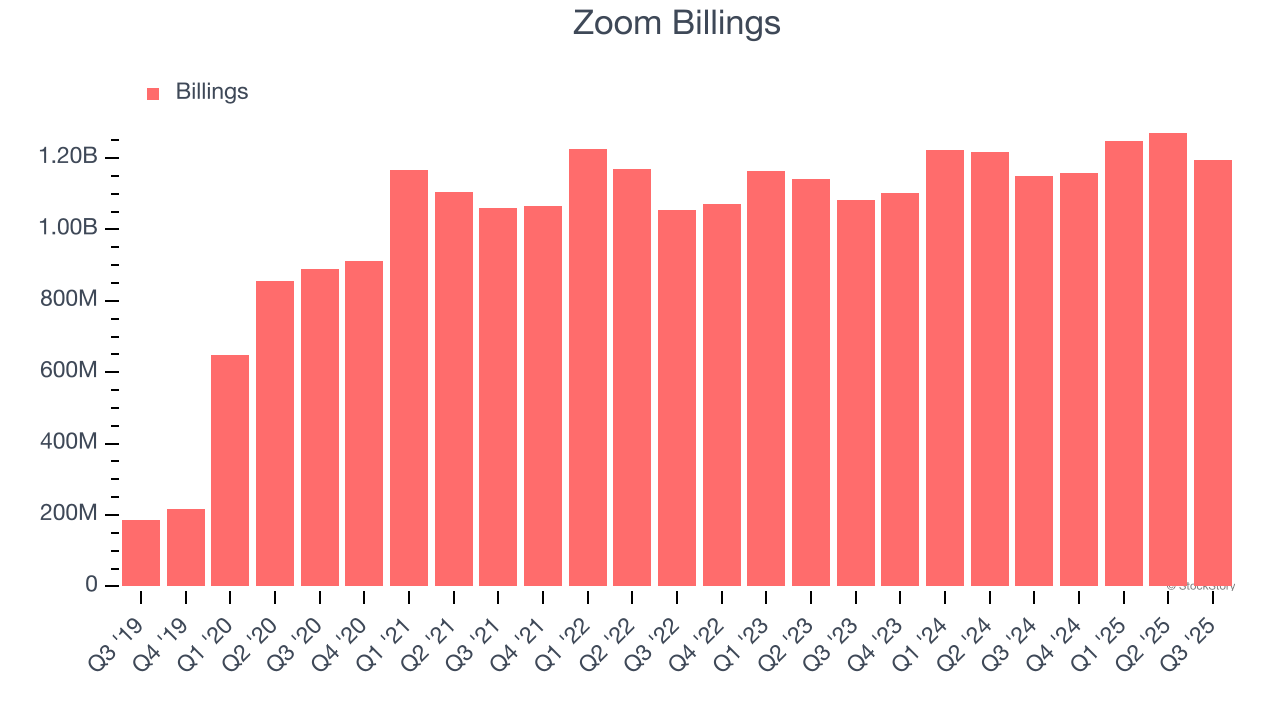

1. Weak Billings Point to Soft Demand

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Zoom’s billings came in at $1.20 billion in Q3, and over the last four quarters, its year-on-year growth averaged 3.9%. This performance was underwhelming and suggests that increasing competition is causing challenges in acquiring/retaining customers.

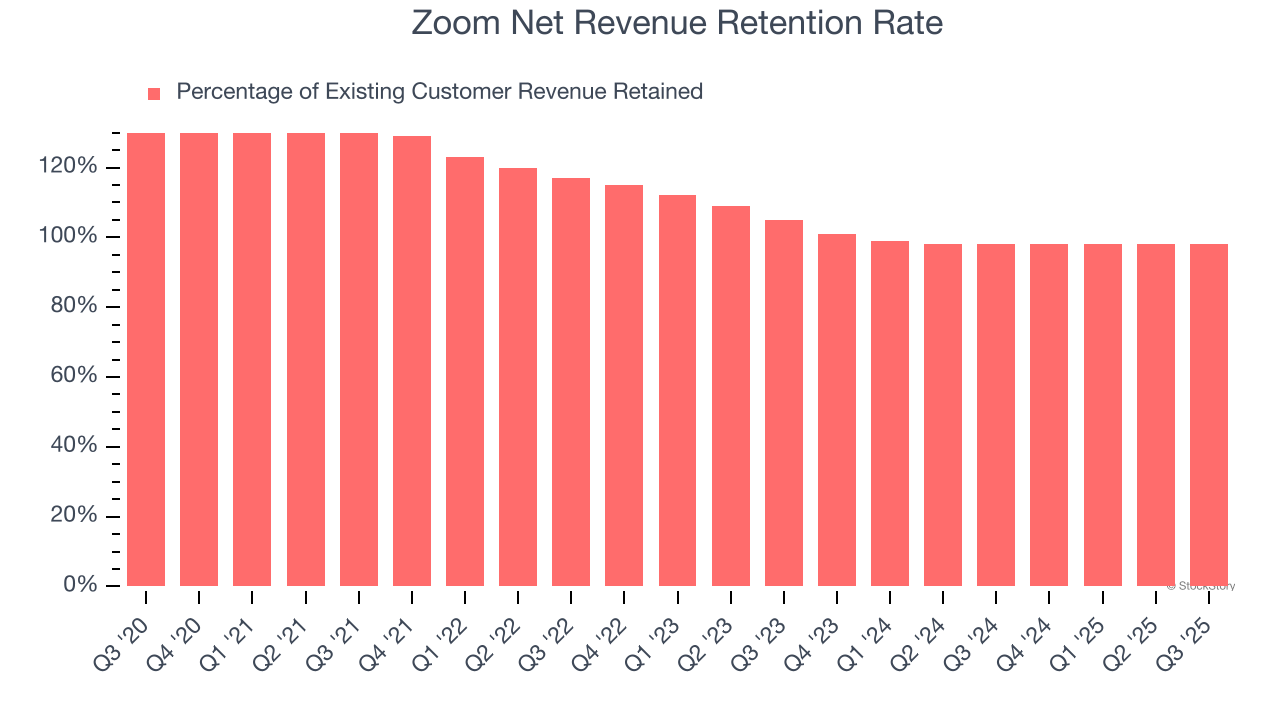

2. Customer Churn Hurts Long-Term Outlook

One of the best parts about the software-as-a-service business model (and a reason why they trade at high valuation multiples) is that customers typically spend more on a company’s products and services over time.

Zoom’s net revenue retention rate, a key performance metric measuring how much money existing customers from a year ago are spending today, was 98% in Q3. This means Zoom’s revenue would’ve decreased by 2% over the last 12 months if it didn’t win any new customers.

Zoom has a weak net retention rate, signaling that some customers aren’t satisfied with its products, leading to lost contracts and revenue streams.

3. Projected Revenue Growth Is Slim

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Zoom’s revenue to rise by 3.6%, close to its 19.7% annualized growth for the past five years. This projection is underwhelming and implies its newer products and services will not accelerate its top-line performance yet.

Final Judgment

We cheer for all companies solving complex business issues, but in the case of Zoom, we’ll be cheering from the sidelines. That said, the stock currently trades at 5.2× forward price-to-sales (or $86.21 per share). This multiple tells us a lot of good news is priced in - we think there are better stocks to buy right now. We’d recommend looking at a top digital advertising platform riding the creator economy.

High-Quality Stocks for All Market Conditions

If your portfolio success hinges on just 4 stocks, your wealth is built on fragile ground. You have a small window to secure high-quality assets before the market widens and these prices disappear.

Don’t wait for the next volatility shock. Check out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.