Quarterly earnings results are a good time to check in on a company’s progress, especially compared to its peers in the same sector. Today we are looking at eXp World (NASDAQ: EXPI) and the best and worst performers in the real estate services industry.

Technology has been a double-edged sword in real estate services. On the one hand, internet listings are effective at disseminating information far and wide, casting a wide net for buyers and sellers to increase the chances of transactions. On the other hand, digitization in the real estate market could potentially disintermediate key players like agents who use information asymmetries to their advantage.

The 13 real estate services stocks we track reported a satisfactory Q1. As a group, revenues beat analysts’ consensus estimates by 2% while next quarter’s revenue guidance was 0.9% below.

In light of this news, share prices of the companies have held steady as they are up 3.9% on average since the latest earnings results.

Weakest Q1: eXp World (NASDAQ: EXPI)

Founded in 2009, eXp World (NASDAQ: EXPI) is a real estate company known for its virtual, cloud-based approach to real estate brokerage.

eXp World reported revenues of $954.9 million, up 1.3% year on year. This print fell short of analysts’ expectations by 4%. Overall, it was a disappointing quarter for the company with a significant miss of analysts’ adjusted operating income estimates.

“We’re entering 2025 from a position of strength. eXp has built one of the most comprehensive, tech-enabled agent value stack in the industry – one that’s driving record International agent productivity and empowering entrepreneurs at scale,” said Glenn Sanford, Founder, Chairman and CEO of eXp World Holdings.

The stock is down 7.7% since reporting and currently trades at $8.

Read our full report on eXp World here, it’s free.

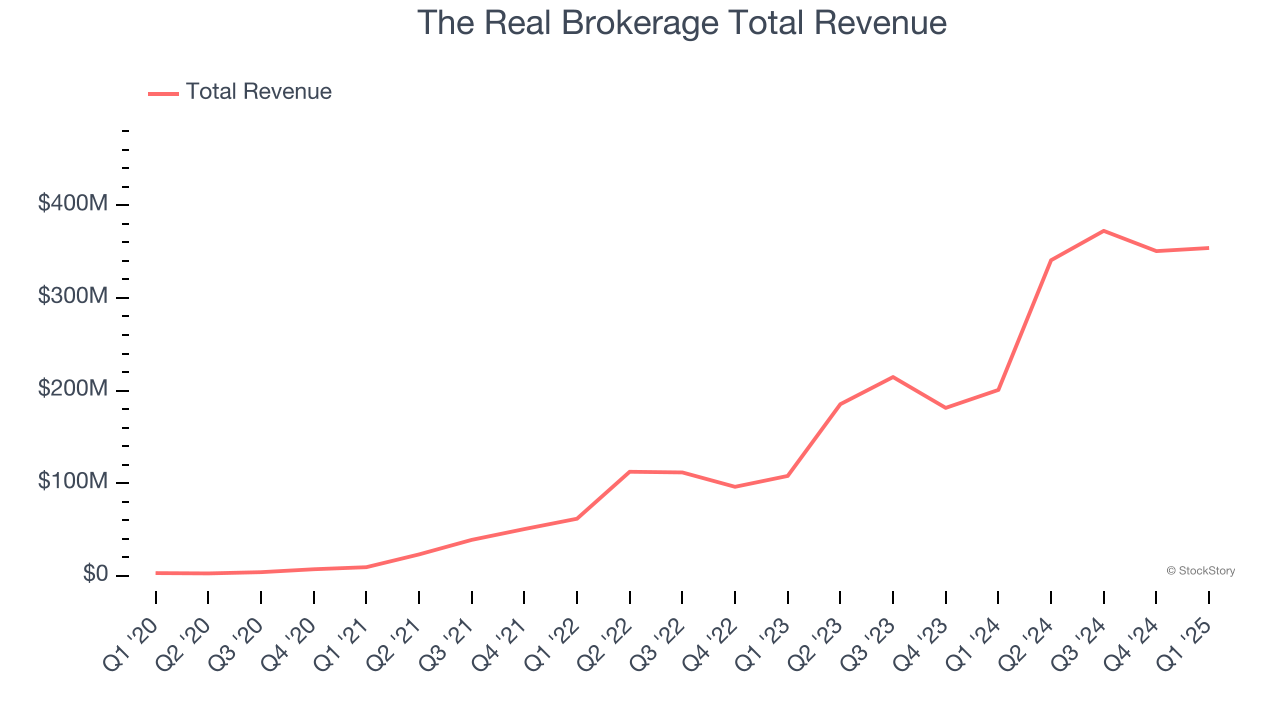

Best Q1: The Real Brokerage (NASDAQ: REAX)

Founded in Toronto, Canada in 2014, The Real Brokerage (NASDAQ: REAX) is a technology-driven real estate brokerage firm combining a tech-centric model with an agent-centric philosophy.

The Real Brokerage reported revenues of $354 million, up 76.3% year on year, outperforming analysts’ expectations by 6.3%. The business had a stunning quarter with an impressive beat of analysts’ EPS estimates and a solid beat of analysts’ EBITDA estimates.

The Real Brokerage pulled off the fastest revenue growth among its peers. However, the results were likely priced into the stock as it’s traded sideways since reporting. Shares currently sit at $4.44.

Is now the time to buy The Real Brokerage? Access our full analysis of the earnings results here, it’s free.

Offerpad (NYSE: OPAD)

Known for giving homeowners cash offers within 24 hours, Offerpad (NYSE: OPAD) operates a tech-enabled platform specializing in direct home buying and selling solutions.

Offerpad reported revenues of $160.7 million, down 43.7% year on year, falling short of analysts’ expectations by 3.1%. It was a slower quarter as it posted a miss of analysts’ homes sold estimates and a miss of analysts’ adjusted operating income estimates.

Offerpad delivered the slowest revenue growth in the group. Interestingly, the stock is up 10.5% since the results and currently trades at $1.16.

Read our full analysis of Offerpad’s results here.

CBRE (NYSE: CBRE)

Established in 1906, CBRE (NYSE: CBRE) is one of the largest commercial real estate services firms in the world.

CBRE reported revenues of $8.91 billion, up 12.3% year on year. This result topped analysts’ expectations by 0.6%. It was a very strong quarter as it also logged an impressive beat of analysts’ adjusted operating income estimates and a solid beat of analysts’ EPS estimates.

The stock is up 7.7% since reporting and currently trades at $131.36.

Read our full, actionable report on CBRE here, it’s free.

Cushman & Wakefield (NYSE: CWK)

With expertise in the commercial real estate sector, Cushman & Wakefield (NYSE: CWK) is a global Chicago-based real estate firm offering a comprehensive range of services to clients.

Cushman & Wakefield reported revenues of $2.28 billion, up 4.6% year on year. This print beat analysts’ expectations by 2.5%. Overall, it was a very strong quarter as it also recorded an impressive beat of analysts’ EPS estimates and a solid beat of analysts’ EBITDA estimates.

The stock is up 20% since reporting and currently trades at $10.80.

Read our full, actionable report on Cushman & Wakefield here, it’s free.

Market Update

Thanks to the Fed’s rate hikes in 2022 and 2023, inflation has been on a steady path downward, easing back toward that 2% sweet spot. Fortunately (miraculously to some), all this tightening didn’t send the economy tumbling into a recession, so here we are, cautiously celebrating a soft landing. The cherry on top? Recent rate cuts (half a point in September 2024, a quarter in November) have propped up markets, especially after Trump’s November win lit a fire under major indices and sent them to all-time highs. However, there’s still plenty to ponder — tariffs, corporate tax cuts, and what 2025 might hold for the economy.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Quality Compounder Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.