Since April 2020, the S&P 500 has delivered a total return of 121%. But one standout stock has nearly doubled the market - over the past five years, Expedia has surged 231% to $161.01 per share. Its momentum hasn’t stopped as it’s also gained 9.6% in the last six months thanks to its solid quarterly results, beating the S&P by 12.9%.

Is now still a good time to buy EXPE? Or are investors being too optimistic? Find out in our full research report, it’s free.

Why Does EXPE Stock Spark Debate?

Originally founded as a part of Microsoft, Expedia (NASDAQ: EXPE) is one of the world’s leading online travel agencies.

Two Positive Attributes:

1. Room Nights Booked Skyrocket, Fueling Growth Opportunities

As an online travel company, Expedia generates revenue growth by increasing both the number of stays (or experiences) booked and the commission charged on those bookings.

Over the last two years, Expedia’s room nights booked, a key performance metric for the company, increased by 11% annually to 86.4 million in the latest quarter. This growth rate is strong for a consumer internet business and indicates people love using its offerings.

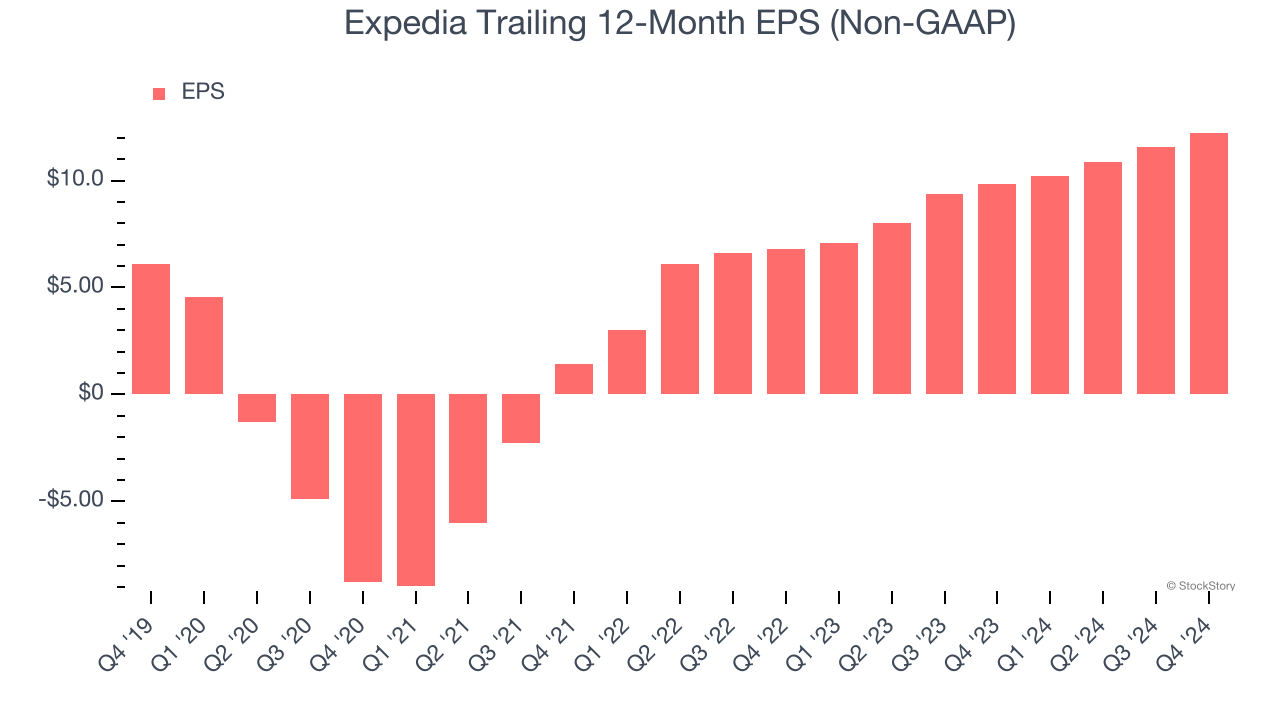

2. Outstanding Long-Term EPS Growth

We track the change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Expedia’s EPS grew at an astounding 104% compounded annual growth rate over the last three years, higher than its 16.8% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

One Reason to be Careful:

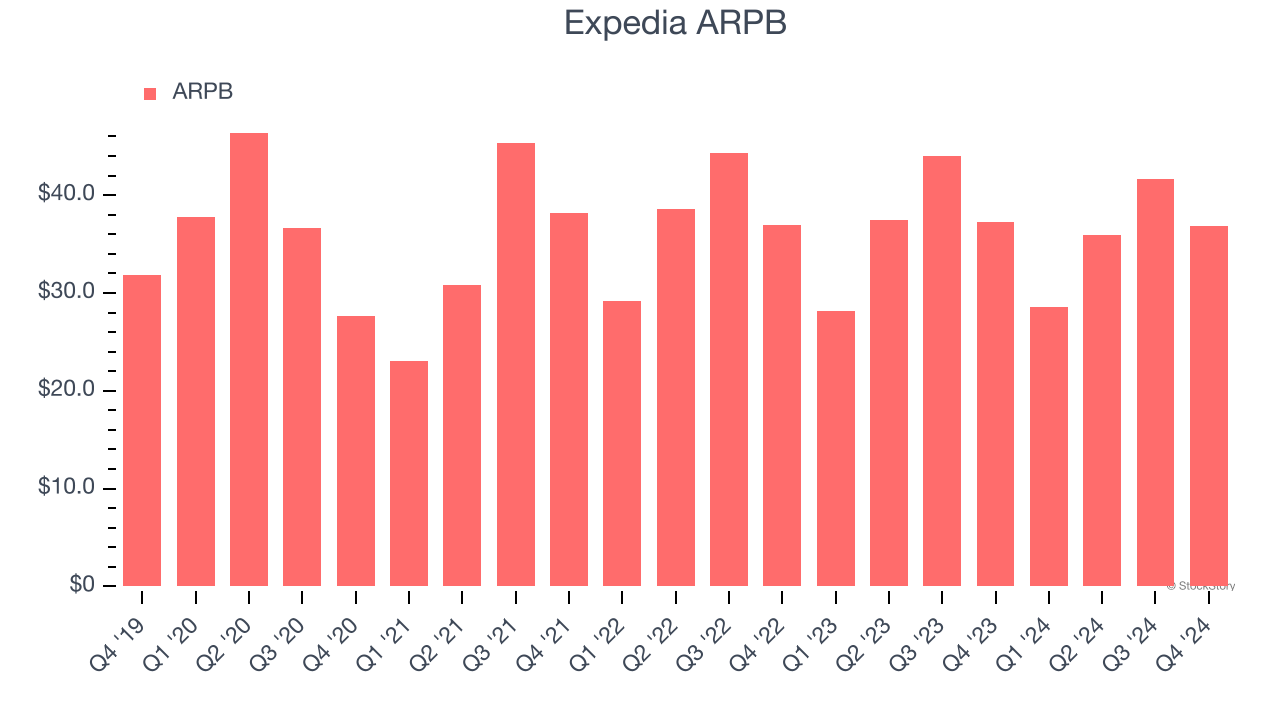

Customer Spending Decreases, Engagement Falling?

Average revenue per booking (ARPB) is a critical metric to track because it not only measures how much users book on its platform but also the commission that Expedia can charge.

Expedia’s ARPB fell over the last two years, averaging 1.9% annual declines. This isn’t great, but the increase in room nights booked is more relevant for assessing long-term business potential. We’ll monitor the situation closely; if Expedia tries boosting ARPB by taking a more aggressive approach to monetization, it’s unclear whether bookings can continue growing at the current pace.

Final Judgment

Expedia’s merits more than compensate for its flaws, and with its shares outperforming the market lately, the stock trades at 7.3× forward EV-to-EBITDA (or $161.01 per share). Is now a good time to buy? See for yourself in our full research report, it’s free.

Stocks We Like Even More Than Expedia

Market indices reached historic highs following Donald Trump’s presidential victory in November 2024, but the outlook for 2025 is clouded by new trade policies that could impact business confidence and growth.

While this has caused many investors to adopt a "fearful" wait-and-see approach, we’re leaning into our best ideas that can grow regardless of the political or macroeconomic climate. Take advantage of Mr. Market by checking out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Sterling Infrastructure (+1,096% five-year return). Find your next big winner with StockStory today for free.