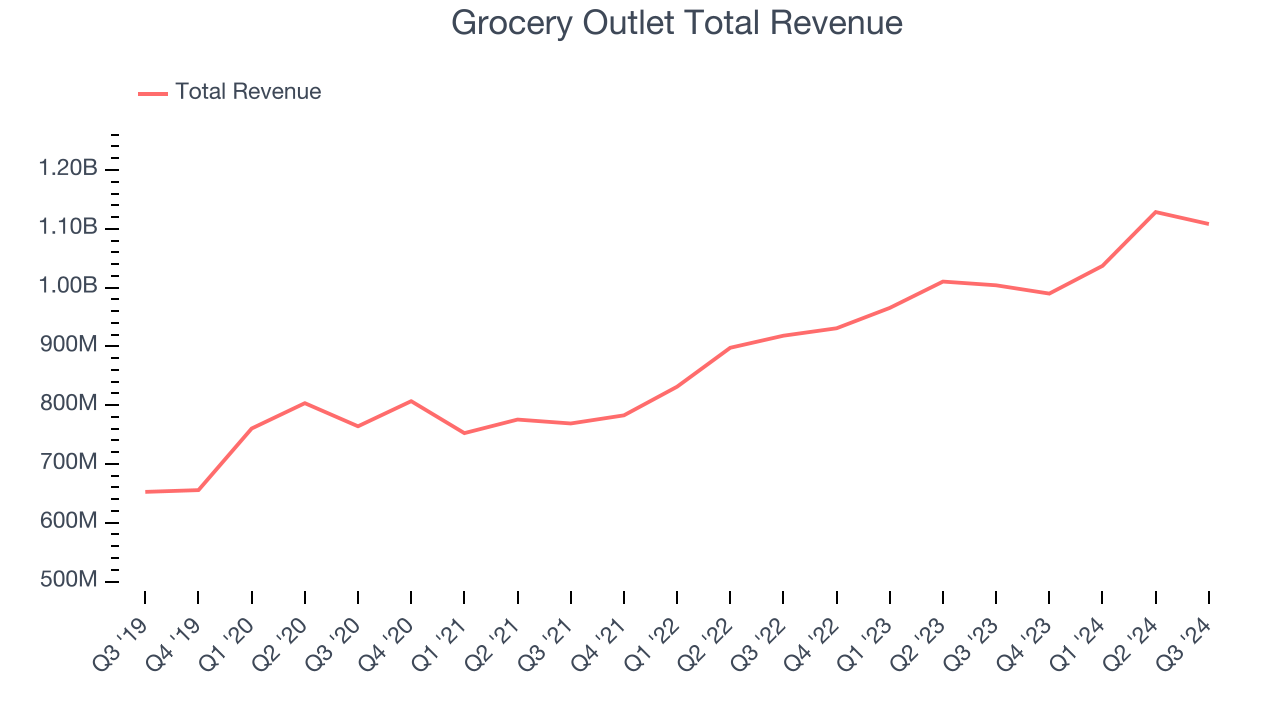

Discount grocery store chain Grocery Outlet (NASDAQ: GO) met Wall Street’s revenue expectations in Q3 CY2024, with sales up 10.4% year on year to $1.11 billion. On the other hand, the company’s full-year revenue guidance of $4.35 billion at the midpoint came in slightly below analysts’ estimates. Its non-GAAP profit of $0.28 per share was 3.4% above analysts’ consensus estimates.

Is now the time to buy Grocery Outlet? Find out by accessing our full research report, it’s free.

Grocery Outlet (GO) Q3 CY2024 Highlights:

- Revenue: $1.11 billion vs analyst estimates of $1.11 billion (in line)

- Adjusted EPS: $0.28 vs analyst estimates of $0.27 (beat by $0.01)

- EBITDA: $72.26 million vs analyst estimates of $70.35 million (2.7% beat)

- The company slightly lifted its revenue guidance for the full year to $4.35 billion at the midpoint from $4.33 billion

- Management lowered its full-year Adjusted EPS guidance to $0.79 at the midpoint, a 14.7% decrease

- EBITDA guidance for the full year is $239.5 million at the midpoint, below analyst estimates of $246.9 million

- Gross Margin (GAAP): 31.1%, in line with the same quarter last year

- Operating Margin: 3.6%, in line with the same quarter last year

- EBITDA Margin: 6.5%, in line with the same quarter last year

- Free Cash Flow Margin: 0%, down from 7.2% in the same quarter last year

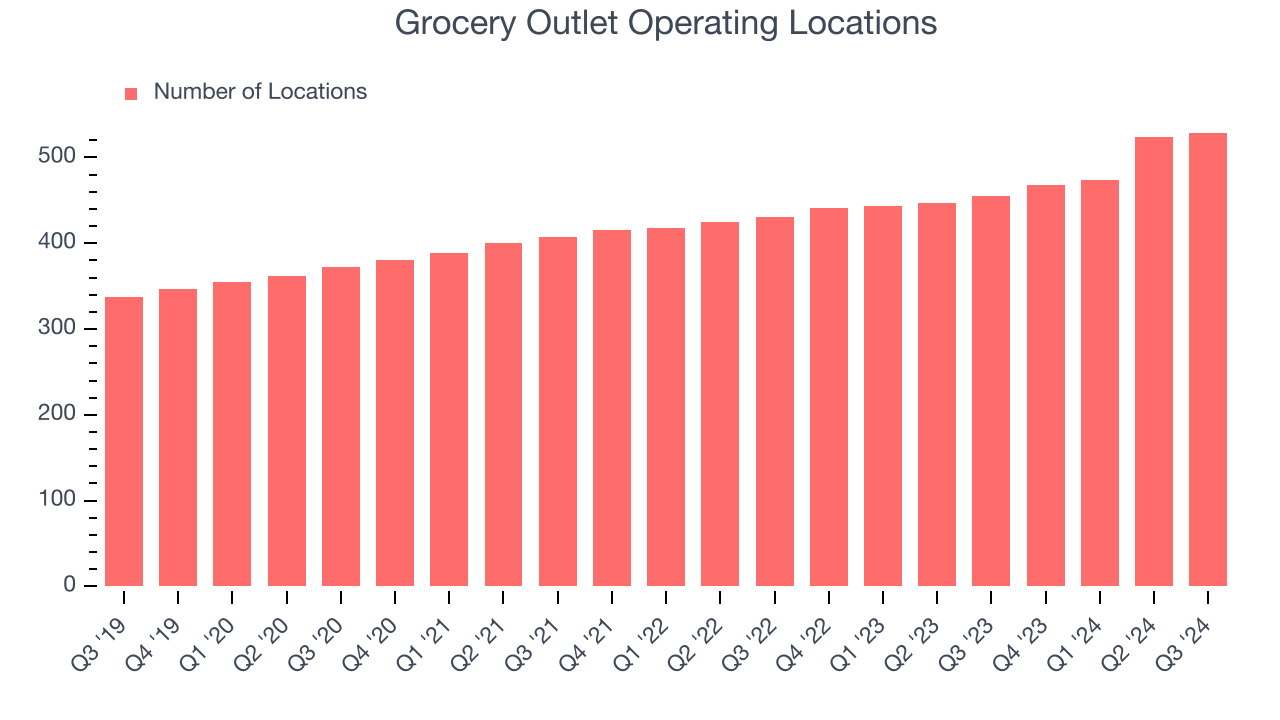

- Locations: 529 at quarter end, up from 455 in the same quarter last year

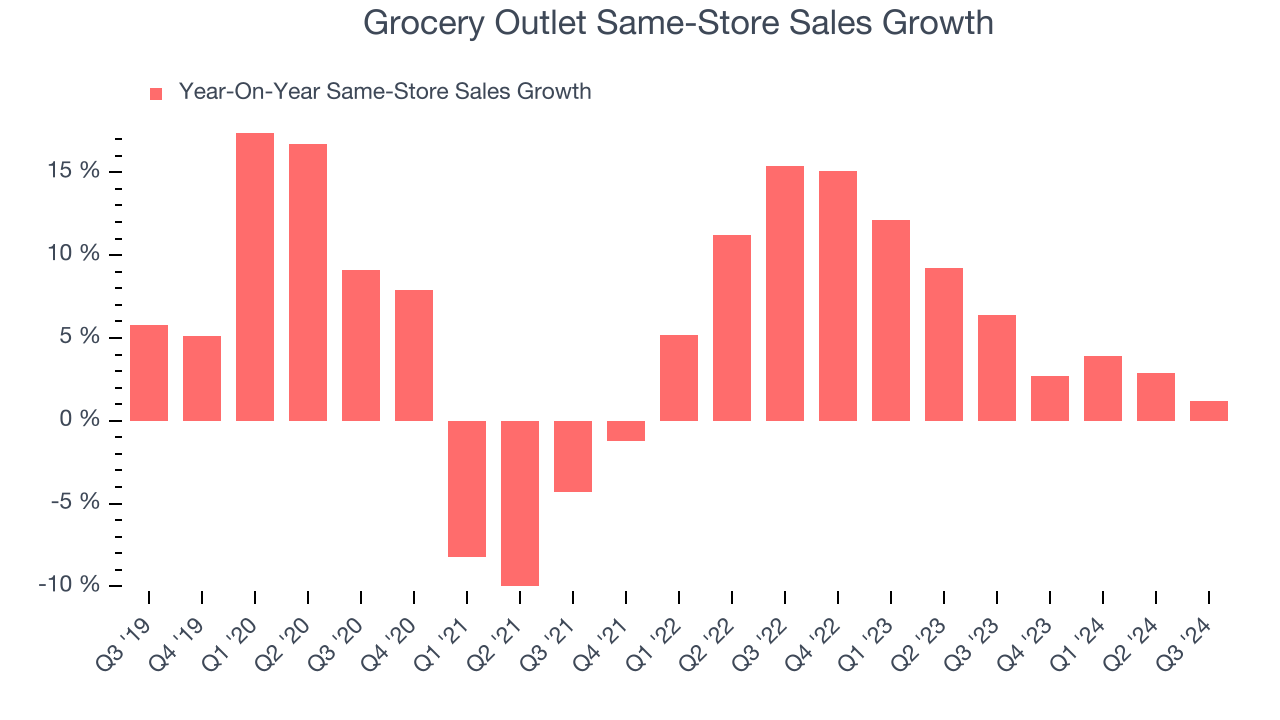

- Same-Store Sales rose 1.2% year on year (6.4% in the same quarter last year) (in line)

- Market Capitalization: $1.41 billion

Eric Lindberg, Chairman and Interim President and CEO of Grocery Outlet said, “Our double-digit third quarter net sales growth reflects the strong positioning of our consumer offering – value continues to win in the market and we continue to grow our share of consumer non-discretionary spending.”

Company Overview

Due to its differentiated procurement and buying approach, Grocery Outlet (NASDAQ: GO) is a discount grocery store chain that offers substantial discounts on name-brand products.

Grocery Store

Grocery stores are non-discretionary because they sell food, an essential staple for life (maybe not that ice cream?). Selling food, however, is a notoriously tough business as grocers must deal with the costs of procuring and transporting oftentimes perishable products. Plus, the costs of operating stores to sell everything from raw meat to ice cream and fresh fruit are high. Competition is also fierce because grocers and other peers such as wholesale clubs tend to sell very similar brands and products. On the bright side, grocery is one of the least penetrated categories in e-commerce because customers prefer to buy their food in person. Still, the online threat exists and will likely increase over time rather than dwindle.

Sales Growth

A company’s long-term performance can give signals about its business quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

Grocery Outlet is a small retailer, which sometimes brings disadvantages compared to larger competitors that benefit from economies of scale.

As you can see below, Grocery Outlet grew its sales at a decent 11.4% compounded annual growth rate over the last five years (we compare to 2019 to normalize for COVID-19 impacts) as it opened new stores and increased sales at existing, established locations.

This quarter, Grocery Outlet’s year-on-year revenue growth was 10.4%, and its $1.11 billion of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 9.3% over the next 12 months, a slight deceleration versus the last five years. This projection is still commendable and shows the market is factoring in success for its products.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Store Performance

Number of Stores

A retailer’s store count often determines how much revenue it can generate.

Grocery Outlet sported 529 locations in the latest quarter. Over the last two years, it has opened new stores at a rapid clip and averaged 8.7% annual growth, among the fastest in the consumer retail sector. This gives it a chance to scale into a mid-sized business over time.

When a retailer opens new stores, it usually means it’s investing for growth because demand is greater than supply, especially in areas where consumers may not have a store within reasonable driving distance.

Same-Store Sales

A company's store base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales gives us insight into this topic because it measures organic growth for a retailer's e-commerce platform and brick-and-mortar shops that have existed for at least a year.

Grocery Outlet has been one of the most successful retailers over the last two years thanks to skyrocketing demand within its existing locations. On average, the company has posted exceptional year-on-year same-store sales growth of 6.7%. This performance suggests its rollout of new stores is beneficial for shareholders. We like this backdrop because it gives Grocery Outlet multiple ways to win: revenue growth can come from new stores, e-commerce, or increased foot traffic and higher sales per customer at existing locations.

In the latest quarter, Grocery Outlet’s same-store sales rose 1.2% annually. By the company’s standards, this growth was a meaningful deceleration from the 6.4% year-on-year increase it posted 12 months ago. We’ll be watching Grocery Outlet closely to see if it can reaccelerate growth.

Key Takeaways from Grocery Outlet’s Q3 Results

Despite in line same-store sales and revenue, Grocery Outlet's EPS narrowly outperformed Wall Street’s estimates. On the other hand, its EBITDA forecast for the full year missed and its full-year EPS guidance was lowered. Overall, this quarter could have been better. The stock remained flat at $14.44 immediately following the results.

Is Grocery Outlet an attractive investment opportunity right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.