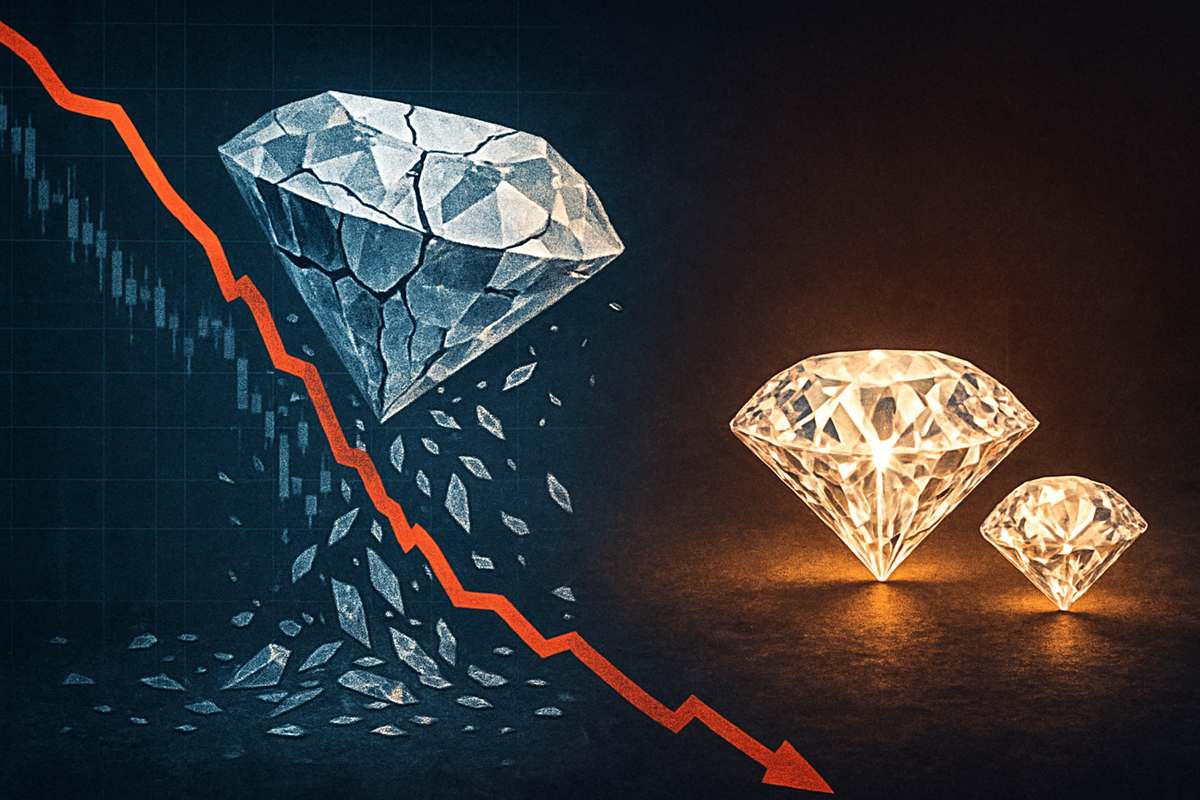

The synthetic diamond market is currently in the throes of a dramatic collapse, with wholesale prices for lab-grown diamonds plummeting by as much as 96% since 2018. This precipitous decline, largely fueled by an overwhelming oversupply and rapid technological advancements in production, is sending shockwaves through the entire global diamond industry. The immediate implications are profound, forcing a fundamental re-evaluation of value propositions, triggering fierce competition for market share, and potentially leading to significant consolidation within the lab-grown sector. While challenging the profitability of synthetic producers, this instability concurrently presents a surprising opportunity for natural diamonds, which are experiencing a renewed surge of consumer interest amidst the volatile landscape of their lab-grown counterparts.

This market upheaval signifies a pivotal moment, as lab-grown diamonds transition from near-premium alternatives to significantly more affordable, mass-market commodities. The long-term effects promise a redefined market structure, altered consumer perceptions, and strategic shifts from all key players, from miners to retailers.

The Great Devaluation: A Deep Dive into the Synthetic Diamond Market Collapse

The scale of the synthetic diamond market's devaluation is stark. Wholesale prices for a one-carat lab-grown diamond, which commanded approximately $4,200 in 2018, have crashed to as low as $168 by 2025 – an astonishing 96% reduction. Two-carat stones have experienced a similar percentage decline. More recently, in the 12 months leading up to November 2024, prices for loose lab-grown diamonds saw a 20% decrease. By 2025, lab-grown diamonds are approximately 83% less expensive than natural diamonds of comparable size and quality, with some industry experts predicting further price drops of 50% to 80%, suggesting the market has yet to find its bottom.

The timeline leading to this collapse is relatively swift. The rapid expansion of manufacturing capabilities, particularly in regions like China and India, has flooded the market with lab-grown gems. This massive oversupply, coupled with continuous advancements in High-Pressure High-Temperature (HPHT) and Chemical Vapor Deposition (CVD) technologies, has made production increasingly efficient and cost-effective. These technological leaps, while beneficial for production scalability, inadvertently stripped producers of pricing power, transforming what was once a controlled luxury item into a mass-produced commodity. The relatively low entry threshold into the lab-grown market initially attracted numerous participants, leading to market saturation and intense competition, forcing companies to continually lower prices to secure sales.

Key players and stakeholders involved span both sides of the diamond divide. In the lab-grown sector, numerous producers, particularly those who invested heavily in scaling production, are now facing severe profitability challenges. On the natural diamond side, major players like De Beers (LSE: DEB) and nations forming the "Luanda Accord" (Angola, Botswana, Democratic Republic of Congo, Namibia, South Africa) are deeply affected. Consumers, whose perceptions of value and authenticity are shifting, are also critical stakeholders.

Initial market reactions have been varied but decisive. The lab-grown industry is grappling with the prospect of significant consolidation, as only the most efficient or vertically integrated grower-manufacturers may survive. There's a growing consensus that lab-grown diamonds are being relegated to the realm of fashion jewelry, losing their competitive edge in the emotionally charged bridal and luxury markets. This shift also undermines consumer trust in synthetic gems as stores of value. Conversely, the instability in the lab-grown market has sparked a resurgence of interest in natural diamonds. The natural diamond industry, which had experienced a price slump since mid-2022, is now seeing renewed appeal. However, the success of lab-grown diamonds has also exerted significant downward pressure on natural diamond prices, which fell by approximately 40% over the past two years. In response, the natural diamond industry is implementing strategic initiatives, such as the Luanda Accord, where major producing nations have agreed to allocate 1% of annual sales revenue towards collective marketing campaigns to promote natural diamonds. Even De Beers (LSE: DEB), a long-standing titan of the natural diamond world, has cut prices for its mined stones and notably launched its own lab-grown brand, Lightbox Jewelry, to adapt to the evolving market dynamics.

Winners and Losers: Navigating the Diamond Industry's New Landscape

The dramatic collapse of the synthetic diamond market is creating a clear delineation of potential winners and losers across the entire diamond industry. Companies heavily invested solely in lab-grown diamond production, particularly those without vertical integration or significant differentiation, are facing immense pressure. Many smaller and less efficient producers are likely to be forced out of the market or acquired, leading to significant consolidation. Their business models, predicated on higher margins that no longer exist, are unsustainable. The perception of lab-grown diamonds as rapidly depreciating fashion accessories, rather than valuable heirlooms, further erodes their long-term market position and consumer confidence.

Conversely, the natural diamond industry, after a period of price adjustments and uncertainty, is showing signs of renewed strength. Companies like De Beers (LSE: DEB) and Alrosa (MCX: ALRS), major natural diamond miners, stand to benefit from the flight to perceived value and authenticity. As the lab-grown market becomes commoditized, the unique, finite, and natural qualities of mined diamonds are being re-emphasized in marketing efforts. This shift could lead to increased demand and potentially stabilize or even improve natural diamond prices in the medium to long term, especially for higher-quality stones. Retailers who successfully pivot their marketing to highlight the distinct value propositions of natural diamonds are also poised to gain.

However, the natural diamond sector is not entirely immune to the ripple effects. The sheer affordability and widespread availability of lab-grown alternatives have fundamentally reset consumer expectations for diamond pricing, putting continued downward pressure on natural diamond prices, particularly for lower-quality or smaller stones. This "cheapening the perception of natural" diamonds could impact the resale value of older mined diamonds. Companies like De Beers (LSE: DEB) that have diversified into lab-grown diamonds with brands like Lightbox Jewelry, while adapting to market trends, also risk diluting their core natural diamond brand if not managed carefully. Ultimately, companies with diversified portfolios, strong brand recognition, and a clear, differentiated value proposition for either natural or specific niches within the lab-grown market are best positioned to navigate this turbulent period.

Wider Significance: A Paradigm Shift in the Diamond World

The collapse of the synthetic diamond market represents more than just a price correction; it signifies a paradigm shift in the broader diamond industry, with far-reaching implications. This event fits into broader industry trends emphasizing sustainability, ethical sourcing, and consumer-driven value. While lab-grown diamonds initially capitalized on these trends with their "conflict-free" narrative, their rapid commoditization now challenges their perceived intrinsic value, forcing a re-evaluation of what consumers truly seek in a diamond purchase. The plummeting prices highlight the inherent difference between a manufactured product with infinite supply potential and a natural rarity.

The ripple effects on competitors and partners are extensive. Jewelry retailers, a crucial link between producers and consumers, must now refine their inventory strategies and marketing messages. Those who previously championed lab-grown diamonds as premium alternatives are now forced to reposition them, potentially alongside fashion jewelry, while simultaneously re-emphasizing the unique allure of natural diamonds. Technology providers for lab-grown production will face reduced demand as manufacturers scale back or consolidate. Furthermore, the event could influence other luxury goods markets, prompting discussions about the sustainability of manufactured alternatives versus natural rarities.

Regulatory or policy implications might emerge as the market stabilizes. There could be increased scrutiny on disclosure and labeling to ensure consumers are fully aware of the origin and characteristics of their diamond purchases. The Federal Trade Commission (FTC) in the United States, for instance, has already updated its guidelines to address the terminology surrounding lab-grown diamonds. International trade bodies may also consider new standards to differentiate and market both categories clearly. Historically, the diamond industry has seen periods of significant disruption, from the discovery of new mines to economic downturns. This current event, however, is unique in that it's driven by technological advancement leading to oversupply of a manufactured alternative, rather than a disruption in the supply of natural stones. It echoes the challenges faced by other industries where technological replication eventually commoditized a previously scarce good, forcing a fundamental re-evaluation of its market position.

What Comes Next: Navigating the Future of Diamonds

The immediate future for the synthetic diamond market suggests continued volatility and consolidation. In the short term, expect more price reductions as producers attempt to offload inventory and unsustainable operations exit the market. Only the most efficient, vertically integrated companies, perhaps those focusing on specific niches or industrial applications where lab-grown diamonds offer superior performance, are likely to survive and eventually thrive. Strategic pivots will be essential, with many lab-grown producers shifting their focus from competing directly with natural diamonds in the luxury bridal market to positioning their products as accessible, fashionable jewelry or industrial materials.

In the long term, the market will likely bifurcate more distinctly. Natural diamonds will solidify their position as rare, investment-grade luxury items, emphasizing their heritage, finite supply, and emotional significance. Lab-grown diamonds, conversely, will increasingly occupy the fashion and accessible luxury segments, appealing to consumers seeking ethical and affordable adornment without the expectation of long-term value retention. This differentiation could lead to a more stable market where both types of diamonds coexist, serving distinct consumer needs.

Market opportunities may emerge for innovators in both sectors. For lab-grown diamonds, this could involve developing new colors, cuts, or applications beyond traditional jewelry, such as in high-tech industries. For natural diamonds, it might involve enhanced traceability, sustainable mining practices, and compelling storytelling that reinforces their unique value. Challenges include managing consumer perception, avoiding a race to the bottom on pricing, and effectively communicating the distinct value propositions of each diamond type. Potential scenarios range from a complete market segmentation, where each diamond type finds its stable niche, to continued price wars that further erode margins across the board, particularly if natural diamond producers react defensively rather than strategically.

Wrap-Up: Reshaping a Timeless Industry

The collapse of the synthetic diamond market is undoubtedly one of the most significant disruptions the diamond industry has witnessed in decades. The key takeaway is the fundamental redefinition of lab-grown diamonds from a luxury alternative to a mass-market commodity, driven by technological advancements and overwhelming oversupply. This event has not only exposed the inherent vulnerability of manufactured scarcity but has also inadvertently revitalized the natural diamond sector, forcing it to reaffirm its unique value proposition of rarity and enduring worth.

Moving forward, the diamond market will be characterized by a clear bifurcation. Natural diamonds will likely reclaim their status as premier symbols of luxury, investment, and emotional significance, while lab-grown diamonds will find their niche in the fashion and affordable jewelry segments. This segmentation, if managed strategically by industry players, could lead to a more stable and transparent market in the long run. The era of direct, head-to-head competition between lab-grown and natural diamonds for the same high-end bridal market appears to be drawing to a close.

Investors should closely watch several indicators in the coming months. These include the pace of consolidation within the lab-grown sector, the effectiveness of marketing campaigns by natural diamond associations (like the Luanda Accord), and any shifts in consumer spending habits between the two categories. The pricing strategies of major players like De Beers (LSE: DEB) for both their natural and lab-grown offerings will also be crucial. Ultimately, the industry is undergoing a profound transformation, and only those companies that adapt swiftly, clearly differentiate their products, and effectively communicate their unique value to consumers will emerge as leaders in this new diamond era.

This content is intended for informational purposes only and is not financial advice