Covered calls at the $200 strike for Chevron Corp (CVX) stock, 5.3% higher, yields 2.1% in one month. Moreover, the 10% higher CVX call strike price yields 1.0% over one month. It may make sense for investors to short out-of-the-money (OTM) puts and calls. This article will show why.

CVX closed at $189.94 on Friday, March 6. That's up slightly from Feb. 27, just +1.7%, right before the Iran war started, when CVX closed at $186.76. So, is CVX stock near a peak?

CVX Price Targets

I discussed shorting out-of-the-money CVX (OTM) puts and calls after Chevron released its Q4 earnings and cash flow, as well as raised its dividend less than expected (Feb. 1 Barchart, "Chevron Hikes Its Dividend - But It's Less Than Expected - Is CVX Stock Fully Valued?').

My price target (PT) was $170 based on its cash flow, and analysts had PTs ranging from $177 to $200. Since then, oil prices have risen to nearly $90 per barrel. That could significantly increase Chevron's future cash flow.

Since then, analysts have raised their PTs, but they are still lower than today's stock price. For example, 26 analysts surveyed by Yahoo! Finance have an average PT of $185.92. That's lower than the March 6 $189.94 closing price.

This is fairly rare, as analysts usually have a higher PT. For example, on Feb. 1, the PT average was $177.67, which over the $176.90 price.

It depends on how long the Iran war will last and whether oil inventories dwindle. However, much of this concern is already discounted by the market.

That's why it makes sense to take advantage of Chevron's high option premiums.

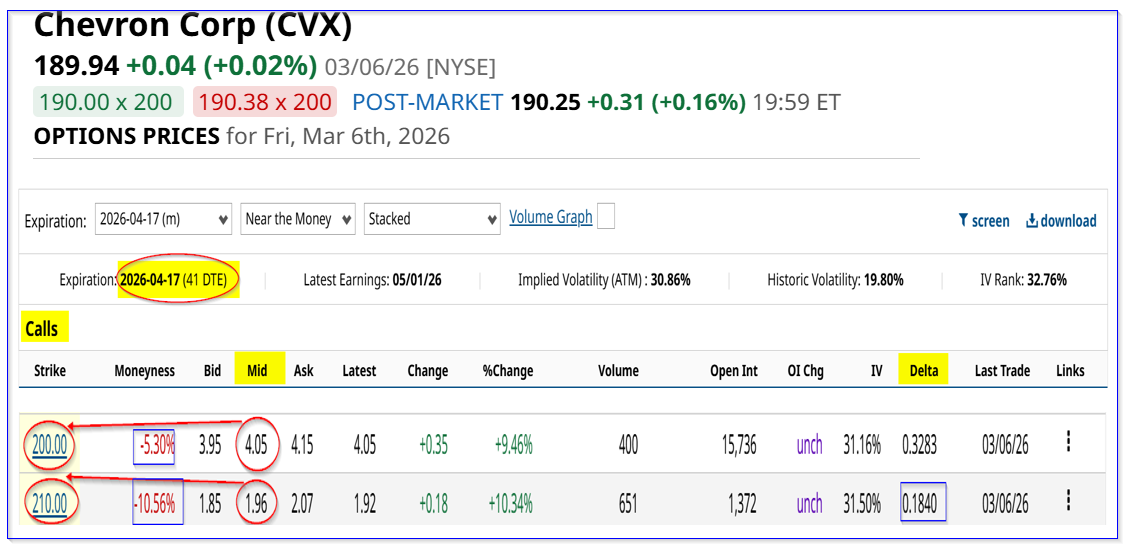

One-Month Covered Calls

This is seen in the April 17, 2026, expiry period. For example, the $200.00 call strike price, which is +5.30% higher than Friday's close, still has a $4.05 midpoint premium.

That implies that a covered call short-seller of these calls can make an immediate one-month yield of 2.13%, after buying 100 shares at $189.94 to cover the short-call:

$405/$18,994 -1 = 0.0213 = 2.13% yield

Moreover, if CVX rises to $200 or higher by April 17, the investor collects an additional 5.3%:

$20,000 / $18,994 -1 = 5.2964%

So, the total return is potentially +7.4264% over the next month.

For investors who are less willing to sell their shares at $200.00, the $210 call price has a midpoint premium of almost $2.00, providing a one-month yield of 1.0%:

$1.96/$189.94 = 1.03%

Note that the delta ratio is lower at 18.4% vs. 32.8% for the $200 call, implying a lower risk of CVX rising to $210 on or before April 17.

That implies that a short-seller who does both calls could average a 1.58% 40 day yield, with another potential 7.93% upside if CVX rises to $207.50.

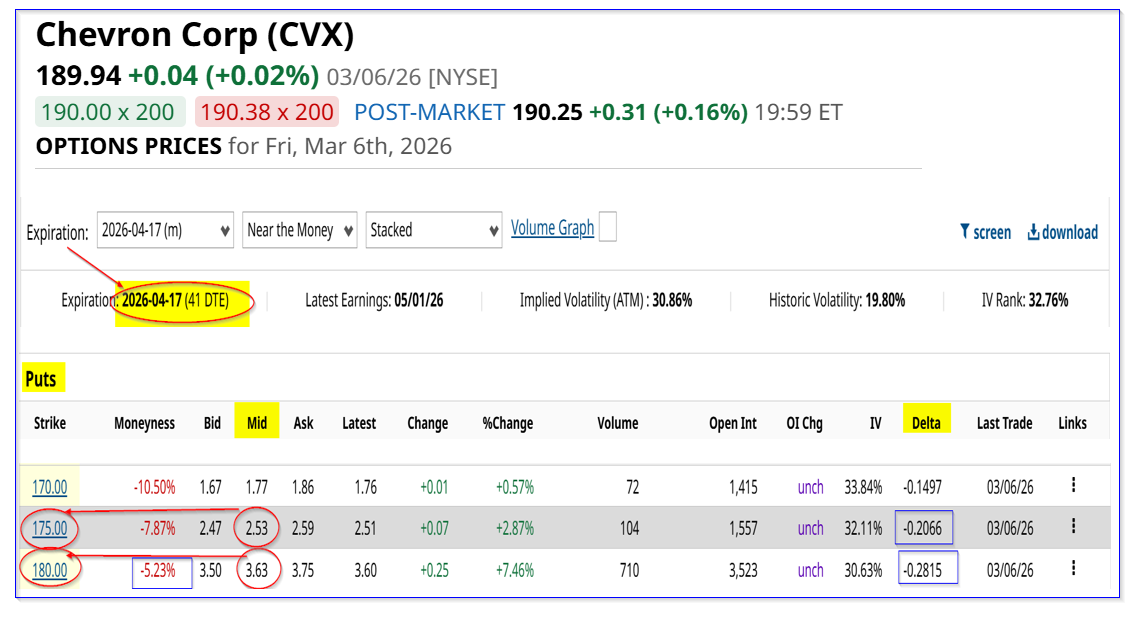

Shorting OTM CVX Puts

Out-of-the-money puts in the same expiry period also have high yields. The only risk here is that an investor would have to buy Chevron shares (not sell them as with covered calls) if CVX fell to the lower strike price.

For example, the April 17, 2026, expiry period shows that the $180.00 strike price put, which is 5.23% lower than Friday's close, has a midpoint premium of $3.63.

That means an investor who secures $18,000 (i.e., less than the covered call buy) can collect $363. That is lower than the $403 collected by the covered call play. But the yield is similar since the cost is lower:

$363/$18,000 -1 = 0.020167 = 2.0167%

That is close to the 2.13% covered call yield at the same distance away (5.30%) from Friday's closing price. However, the delta ratio is much lower at 28% vs. the 32% covered call play.

Moreover, for more risk-averse investors, the $175.00 put offers a 1.45% yield (i.e., $2.53/$175.00) at a much lower delta - 20.7%.

One issue for investors who short these puts is that if CVX rises, they don't gain any upside, as covered call players earn. Moreover, if CVX falls below the strike price, the investor may end up with an unrealized loss. However, they would still own CVX shares.

The bottom line is that CVX covered call plays and out-of-the-money short-put plays have attractive yields. That could be attractive to investors who believe oil is at or near a peak price.

On the date of publication, Mark R. Hake, CFA did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- If Oil Is at a Peak, Does Shorting Chevron Puts and Calls Make Sense?

- The Saturday Spread: Using Microstructure Analytics to Trade Multi-Leg Options

- Unusual Options Activity Suggests the Smart Money Is Bullish About Rio Tinto Stock Despite Glencore Deal Collapse

- Tesla Put Option Premiums are High - Attractive to Short Sellers and Value Investors