Analysts at brokerage firm Wedbush, led by Dan Ives, have been consistent about their bullishness on tech names. In fact, when the market has been clobbering software stocks due to their perceived irrelevance in the age of AI, Ives and his band of analysts have been waving the flag for these names. Thus, it is not surprising that a war in West Asia is not enough to deter their belief in some of the leading names from the tech sector.

In a note to clients, the firm elaborated on its stance further, stating, “These tech names are defensive and well-positioned stocks to navigate this volatility with robust business models. The cybersecurity and military-exposed names (Palantir) are particularly well positioned in our view.”

Considering this view, here are three chosen names among Wedbush's favorites that investors can have a look at now for the long haul.

Stock #1 Apple

We start our list with Apple (AAPL) as the consumer tech giant recently came out with its new set of products. Founded in 1976 by the visionary Steve Jobs, among others, Apple designs and sells consumer electronics, software, and digital services with some of the most recognizable names in the industry, such as iPhone, MacBook, iPad, and iMac. Moreover, over the years, it has built a strong services business as well.

Valued at a market cap of 3.82 trillion, Apple is one of the most valuable companies in the world. However, the stock is down 5.49% year-to-date (YTD).

Regardless of the sentiment on the Street, Apple has been on an estimate-beating spree for more than two years. And the most recent quarter was no different.

For fiscal Q1 2026, Apple reported revenues of $143.8 billion, up 16% from the previous year. This was driven largely by robust demand for the iPhone 17 lineup. iPhone net sales reached $85.3 billion, reflecting a 23% year-over-year (YOY) increase. The high-margin services segment also posted solid growth, with net sales climbing to $30 billion from $26.3 billion in the year-ago period.

Gross margins widened to 48.2%, underscoring the company's pricing discipline and product mix strength. Earnings per share rose 18% to $2.84, surpassing the Street consensus of $2.65. Share repurchases totaled $25.2 billion during the quarter, providing additional support to EPS growth.

Operating cash flow was particularly impressive at $53.9 billion, an 80% increase from the prior year. The company closed the period with $45.3 billion in cash and equivalents, well ahead of short-term debt of $13.8 billion.

However, valuation metrics reflect the premium placed on Apple's growth profile. The stock currently trades at a forward P/E of 31.22x, P/S of 8.22x, and P/CF of 26.20x. These are all above the sector medians of 21.82x, 3.08x, and 17.57x, respectively.

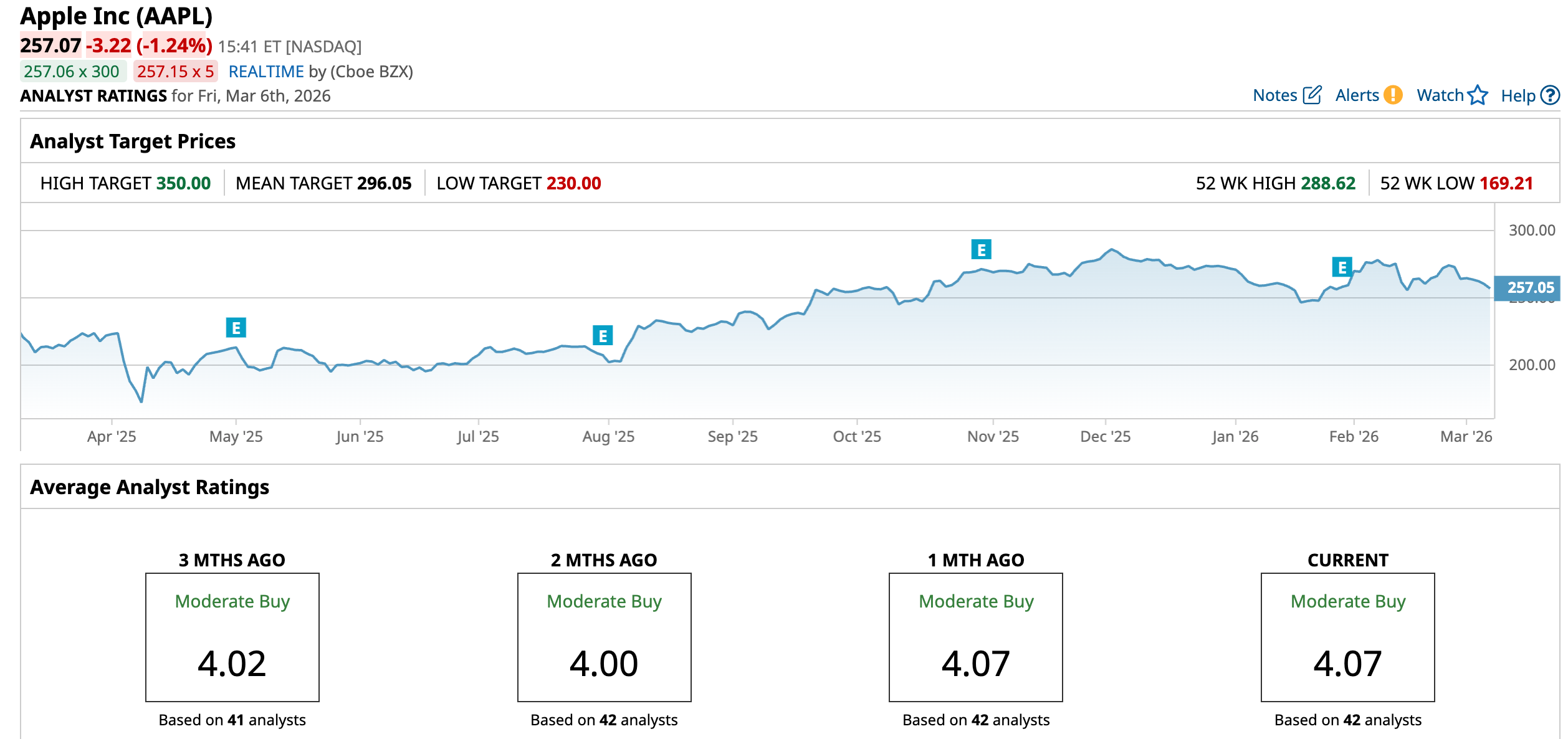

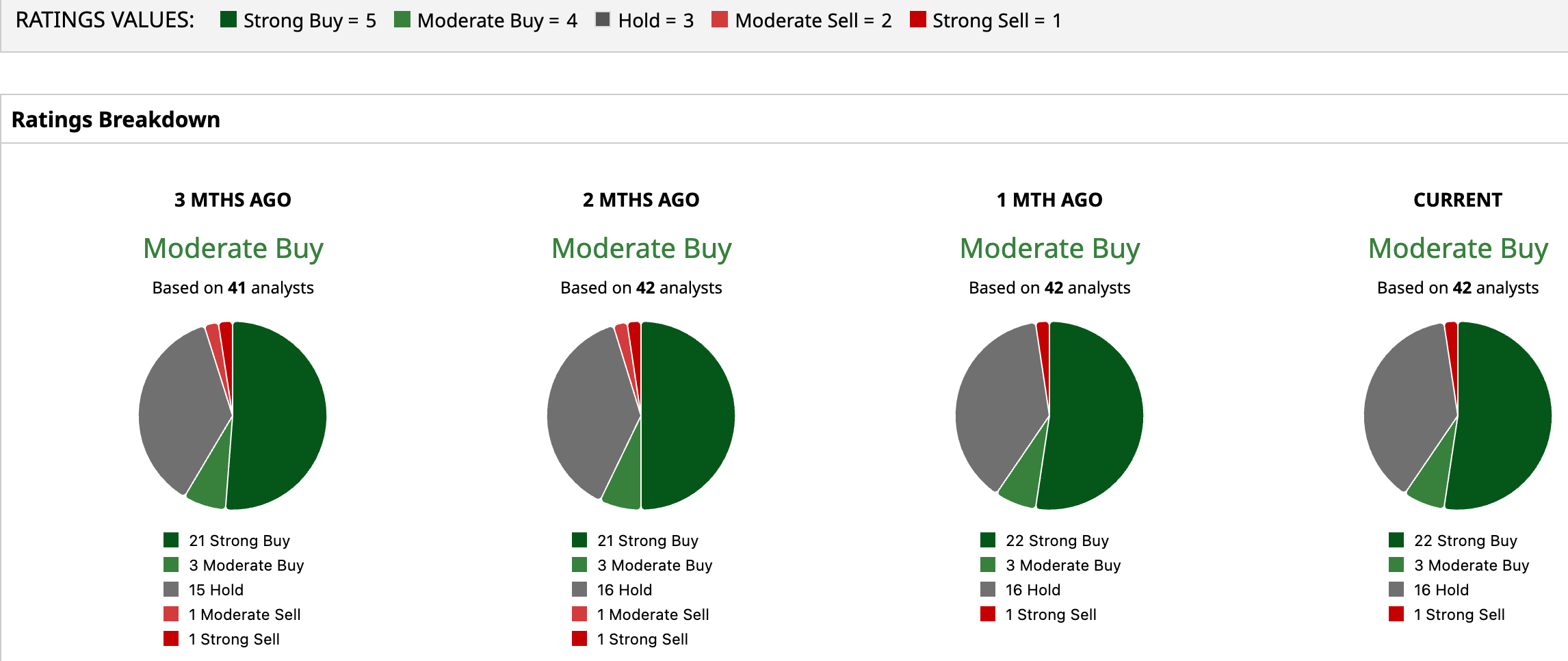

Overall, analysts have an overall rating of “Moderate Buy” for the stock, with the mean target price of $296.05. This implies an upside of 15.16% from current levels. Out of 42 analysts covering the stock, 22 have a “Strong Buy” rating, three have a “Moderate Buy” rating, 16 have a “Hold” rating, and one has a “Strong Sell” rating.

Stock #2 Microsoft

We move on to another Ives favorite, Microsoft (MSFT). Co-founded in 1975 by Bill Gates, Microsoft is one of the largest and most diversified technology companies globally, with instantly recognizable names such as Microsoft 365, Azure, and Xbox in its stable. Microsoft also invests heavily in AI (Copilot services, Azure AI), cybersecurity tools, and developer platforms.

Valued at about $3 trillion, Microsoft is one of the most valuable companies in the world and was one of the first investors in AI bellwether OpenAI. Yet, like its smaller peers in the software space, the MSFT stock has had a troubled 2026 so far, falling 15.39% YTD.

Notably, Microsoft's most recent quarter (ended December 31, 2025) delivered another set of strong results, with both revenue and earnings comfortably exceeding analyst expectations.

Total revenue came in at $81.3 billion, reflecting a 16.7% YOY increase. The cloud segment remained a standout, growing 26% to $51.5 billion. Meanwhile, earnings per share rose 28.2% to $4.14, well ahead of the $3.91 consensus estimate. This marked the company's ninth consecutive quarter of beating bottom line forecasts.

Operating cash flow showed significant strength as well, rising 60.5% to $35.8 billion from the year-ago period. The company ended the quarter with $24.3 billion in cash and equivalents, substantially ahead of its $4.8 billion in short-term debt.

Yet, the stock continues to trade at overvalued levels. Its forward P/E, P/S, and P/CF of 24.75x, 9.30x, and 18.66x are all above the sector medians of 21.82x, 3.08x, and 17.57x, respectively.

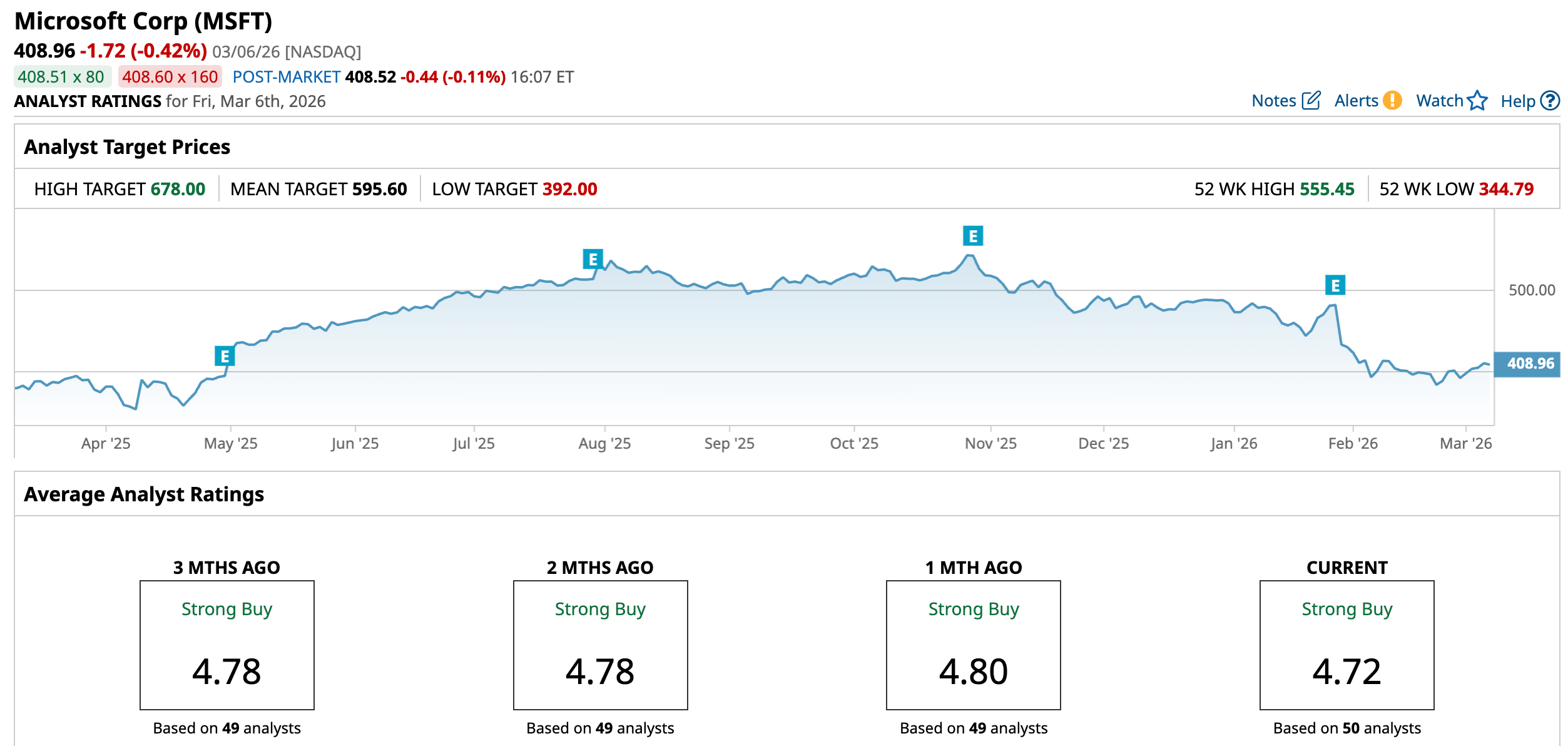

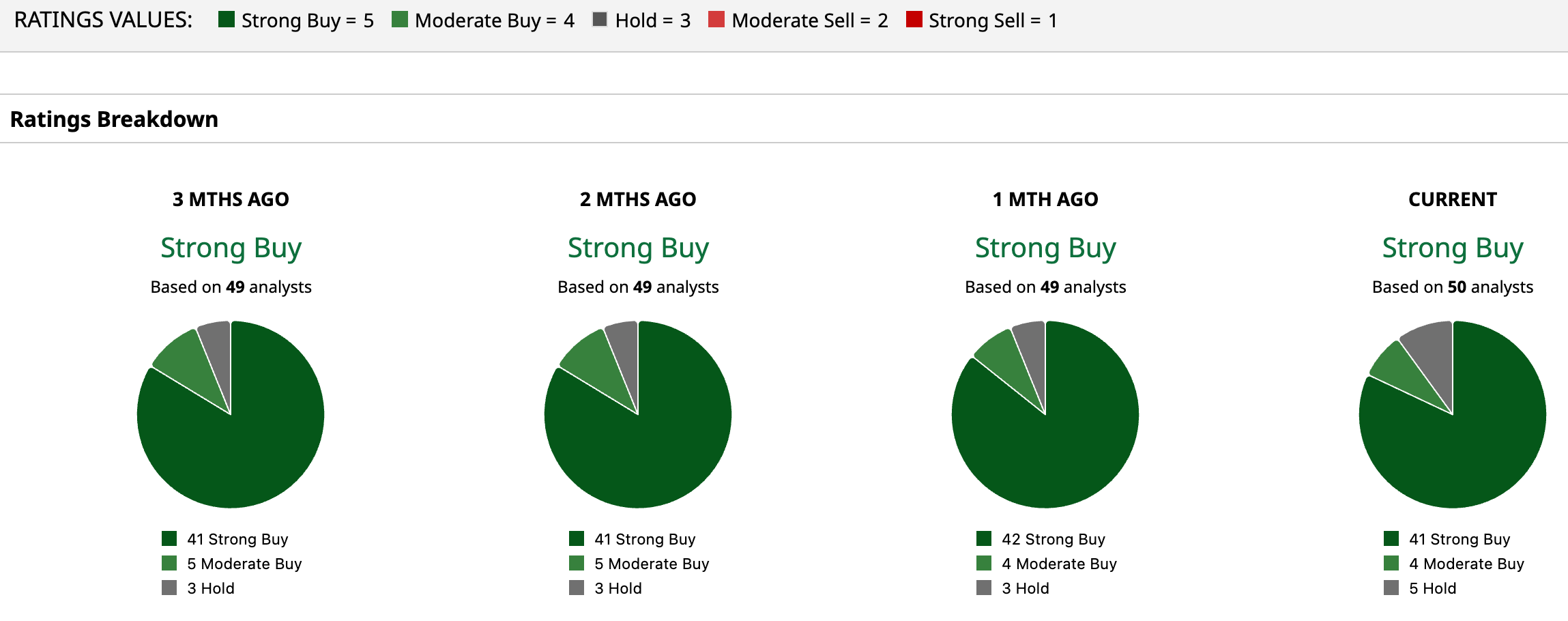

Meanwhile, analyst sentiment remains firmly positive. The stock carries a consensus “Strong Buy” rating, with a mean price target of $595.60, implying roughly 45.64% upside from current levels. Of the 50 analysts covering MSFT, 41 assign a “Strong Buy,” four rate it “Moderate Buy,” and five maintain a “Hold.”

Stock #3 ServiceNow

Now, we conclude our list with ServiceNow (NOW). Founded in 2004, ServiceNow provides a cloud platform that automates digital workflows across enterprises. Its flagship product is the Now Platform, which allows companies to automate and manage operational processes across departments.

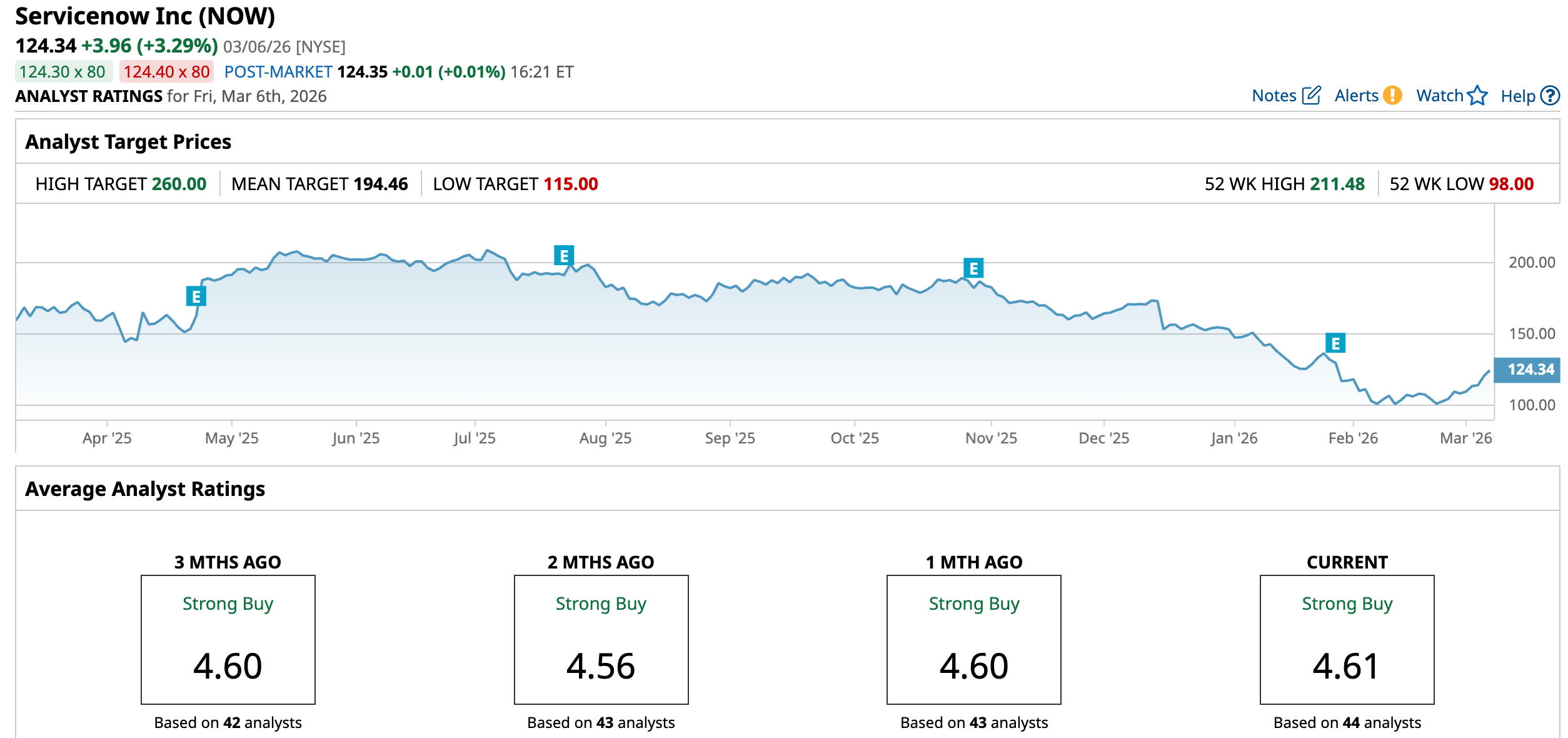

Its market cap currently stands at $125.9 billion, while its stock is down 18.85% YTD.

However, despite all the hue and cry about software stocks in the market, ServiceNow's results for the most recent quarter exceeded expectations on both the bottom line and the top line. Total revenues for the quarter came in at $3.6 billion, up 20.5% from the previous year. Within this, the core segment of subscription revenues went up by 21% YOY to $3.5 billion.

Further, earnings increased by an even more 25.3% in the same period to $0.92 per share, higher than the consensus estimate of $0.89 per share. Notably, this was the ninth consecutive quarter of earnings beat from the company.

Additionally, remaining performance obligations, a key metric used to gauge the demand visibility, grew at a healthy pace of 26.5% from the prior year to $28.2 billion.

Coming to cash flows, net cash from operating activities for the quarter came in at $2.2 billion, up from $1.6 billion in the year-ago period. Overall, the company closed the quarter with a cash balance of $3.7 billion, which was much higher than its short-term debt levels of just $112 million.

However, even after such a stark drawdown in the share price, ServiceNow continues to trade at elevated levels. Its forward P/E, P/S, and P/CF of 28.92x, 7.88x, and 19.6x are all above the sector medians of 21.82x, 3.08x, and 17.57x, respectively.

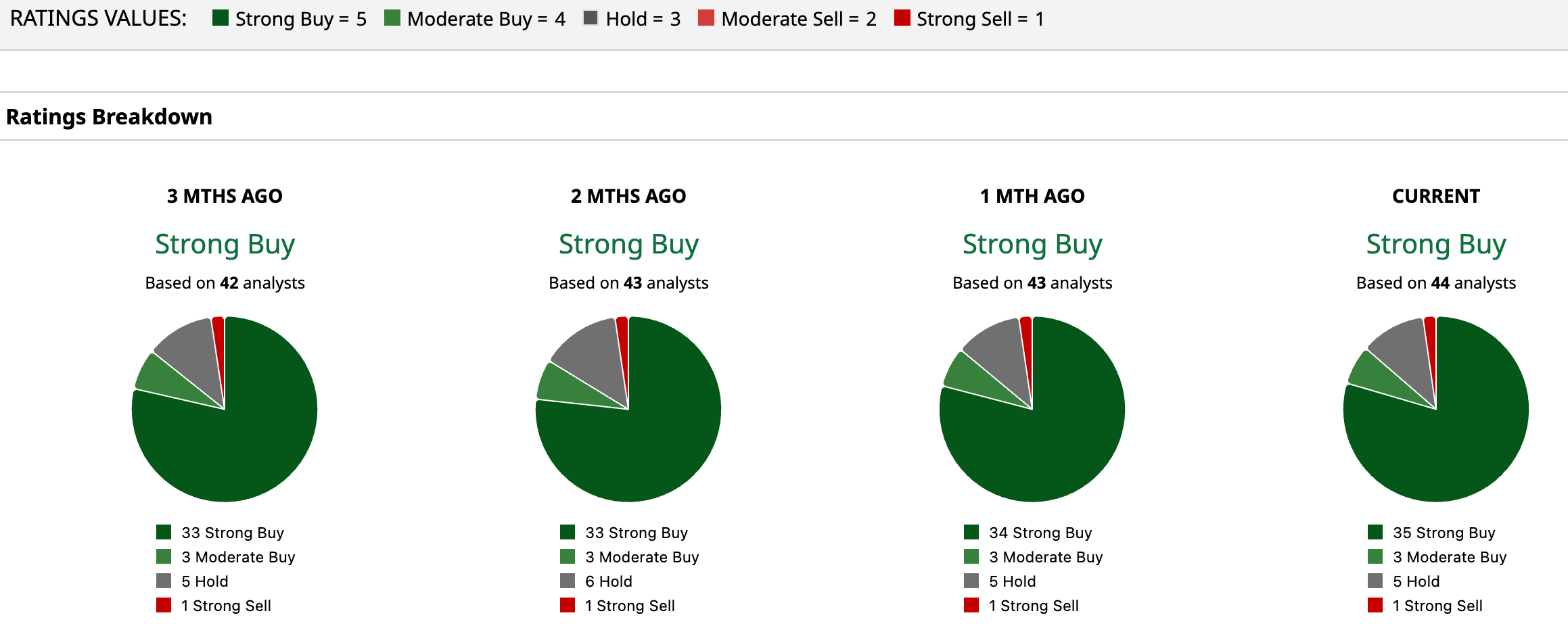

Taking all of this into account, analysts have attributed an overall rating of “Strong Buy” for the stock, with a mean target price of $194.46, which denotes an upside potential of about 56.4% from current levels. Out of 44 analysts covering the stock, 35 have a “Strong Buy” rating, three have a “Moderate Buy” rating, five have a “Hold” rating, and one has a “Strong Sell” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- ‘When You See One Cockroach, There are Probably More’: Blackrock Forced to Halt Redemptions As $2 Trillion Private Lending Bubble Starts Showing Cracks

- Analysts Say These Are the Top 3 Stocks to Buy Amid the U.S.-Israel War on Iran

- If Oil Is at a Peak, Does Shorting Chevron Puts and Calls Make Sense?

- 1 Little-Known Tech Stock That Wedbush Calls a Must-Own Amid Middle East Conflict