Based in Cleveland, Ohio, TransDigm Group Incorporated (TDG) designs, manufactures, and supplies highly engineered aircraft components. It delivers actuators, ignition systems, connectors, cockpit displays, safety restraints, and testing solutions to aerospace manufacturers, airlines, military agencies, and industrial equipment producers worldwide.

With a market cap of nearly $73.6 billion, TransDigm occupies the “large-cap” territory, a class reserved for companies valued above $10 billion. The scale strengthens the company’s purchasing leverage, supports disciplined acquisitions, and enables consistent investment in engineering and compliance.

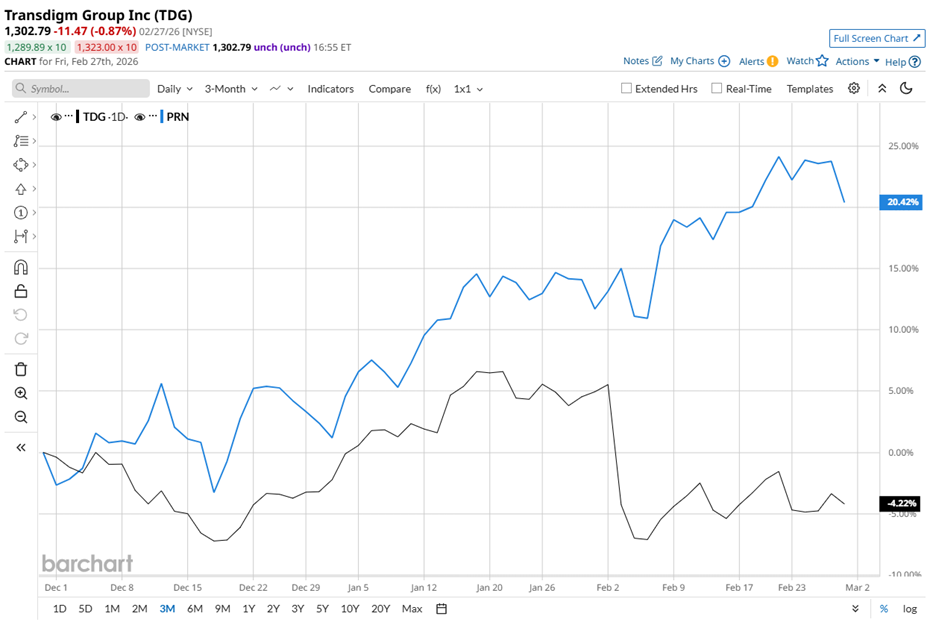

TDG stock is currently trading 19.8% below its 52-week high of $1,623.82 reached in July 2025. Over the past three months, the stock has declined 3.9%. During the same period, the Invesco Dorsey Wright Industrials Momentum ETF (PRN) gained 21.6%, signaling that investors have favored broader industrial exposure, while TransDigm has moved sideways to lower.

The longer-term view tells a similar story. Over the past 52 weeks, TDG stock has slipped 3.5% and declined 2% year-to-date (YTD). In contrast, PRN surged 42.4% over the last 52 weeks and advanced 19% in 2026.

From a technical perspective, the stock briefly traded above its 50-day and 200-day moving averages in January. However, the momentum did not hold. In February, TDG stock fell below both key indicators. It now trades under its 50-day moving average of $1,346.76 and its 200-day moving average of $1,380.64.

The sharpest pullback followed TransDigm’s Q1 2026 financial results, reported on Feb. 3. The stock fell 9.3% that day as investors reassessed premium valuation levels and execution risks tied to OEM production ramp rates.

Capital allocation also drew scrutiny. TransDigm announced pending acquisitions of Stellant Systems for approximately $960 million and Jet Parts Engineering and Victor Sierra Aviation for about $2.2 billion. Investors evaluated integration risk and the potential for near-term EBITDA margin dilution from these transactions.

Operational performance, however, remained solid. Revenue rose 13.9% year over year to $2.29 billion, exceeding the Street’s forecasts of $2.25 billion. Adjusted EPS increased 5.1% to $8.23, above analyst expectations of $8.02. The company generated over $830 million in operating cash flow and ended with more than $2.5 billion in cash.

To sharpen the comparison, TransDigm’s rival General Dynamics Corporation (GD) has delivered a 41.9% gain over the past 52 weeks and a 6.1% rise YTD. The outperformance sets a demanding benchmark. It also highlights the performance gap TransDigm can still close if execution aligns with expectations.

Wall Street has not turned cautious. Among 22 analysts covering the stock, the consensus rating stands at a “Moderate Buy.” To that end, the average price target of $1,594.79 implies potential upside of 22.4% from current levels, reinforcing constructive sentiment.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart