Let’s dig into the relative performance of Paycom (NYSE: PAYC) and its peers as we unravel the now-completed Q2 hr software earnings season.

Modern HR software has two powerful benefits: cost savings and ease of use. For cost savings, businesses large and small much prefer the flexibility of cloud-based, web-browser-delivered software paid for on a subscription basis rather than the hassle and complexity of purchasing and managing on-premise enterprise software. On the usability side, the consumerization of business software creates seamless experiences whereby multiple standalone processes like payroll processing and compliance are aggregated into a single, easy-to-use platform.

The 5 HR software stocks we track reported a slower Q2. As a group, revenues beat analysts’ consensus estimates by 0.5% while next quarter’s revenue guidance was 2.7% below.

In light of this news, share prices of the companies have held steady. On average, they are relatively unchanged since the latest earnings results.

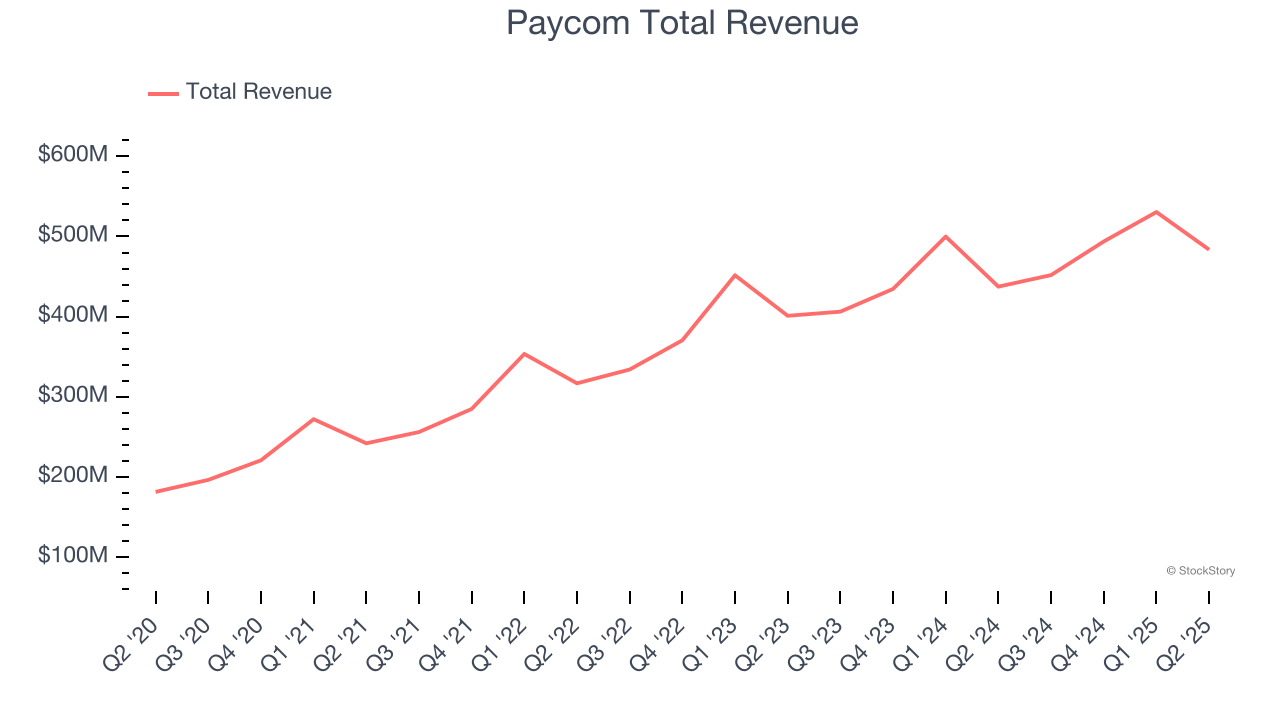

Best Q2: Paycom (NYSE: PAYC)

Pioneering the concept of employees doing their own payroll with its "Beti" technology, Paycom (NYSE: PAYC) provides cloud-based human capital management software that helps businesses manage the entire employment lifecycle from recruitment to retirement.

Paycom reported revenues of $483.6 million, up 10.5% year on year. This print exceeded analysts’ expectations by 2.5%. Overall, it was a very strong quarter for the company with an impressive beat of analysts’ EBITDA estimates and full-year EBITDA guidance exceeding analysts’ expectations.

Unsurprisingly, the stock is down 1.7% since reporting and currently trades at $219.02.

Is now the time to buy Paycom? Access our full analysis of the earnings results here, it’s free.

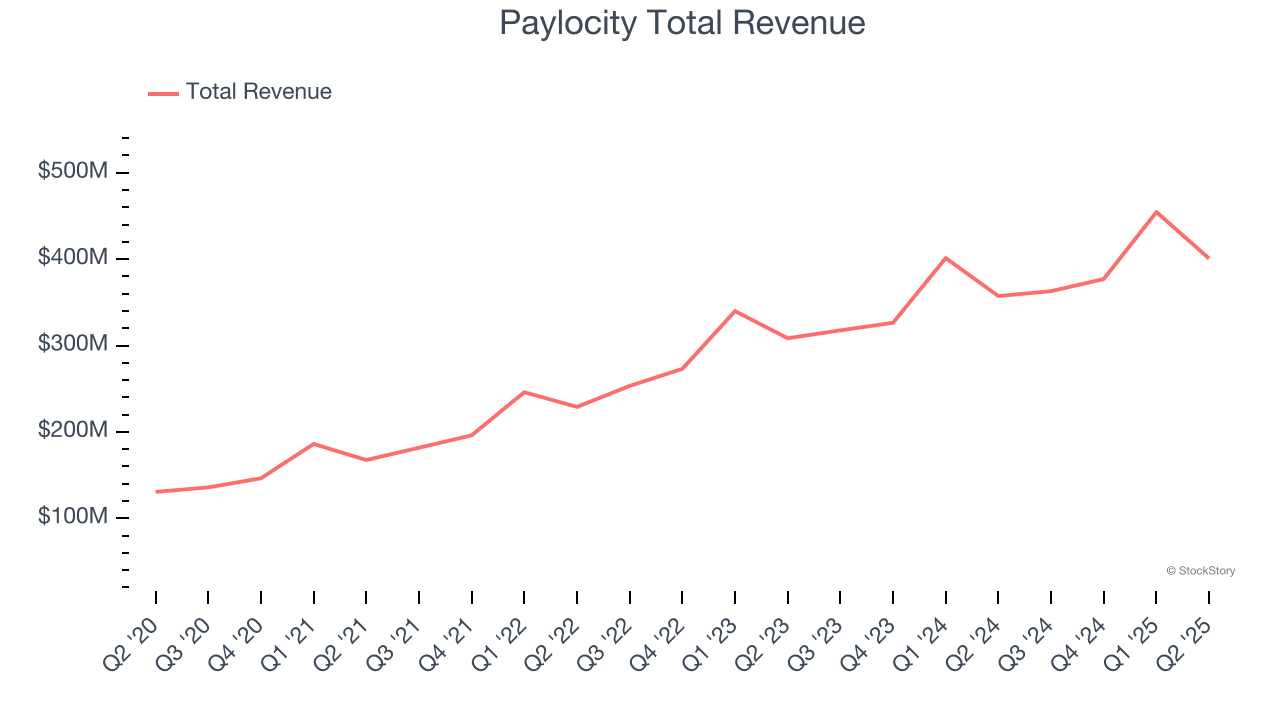

Paylocity (NASDAQ: PCTY)

Operating in a field where companies traditionally juggled multiple disconnected systems, Paylocity (NASDAQ: PCTY) provides cloud-based human capital management and payroll software solutions that help businesses manage their workforce and HR processes.

Paylocity reported revenues of $400.7 million, up 12.2% year on year, outperforming analysts’ expectations by 3.1%. The business had a satisfactory quarter with a solid beat of analysts’ EBITDA estimates but full-year guidance of slowing revenue growth.

Paylocity scored the biggest analyst estimates beat and fastest revenue growth among its peers. Although it had a fine quarter compared its peers, the market seems unhappy with the results as the stock is down 4.1% since reporting. It currently trades at $174.22.

Is now the time to buy Paylocity? Access our full analysis of the earnings results here, it’s free.

Weakest Q2: Paychex (NASDAQ: PAYX)

Once known as the go-to service for small business payroll needs, Paychex (NASDAQ: PAYX) provides payroll processing, HR services, employee benefits administration, and insurance solutions to small and medium-sized businesses.

Paychex reported revenues of $1.43 billion, up 10.2% year on year, falling short of analysts’ expectations by 1.1%. It was a disappointing quarter as it posted a miss of analysts’ EBITDA estimates.

As expected, the stock is down 11.2% since the results and currently trades at $135.20.

Read our full analysis of Paychex’s results here.

Dayforce (NYSE: DAY)

Rebranded from Ceridian in January 2024 to highlight its flagship product, Dayforce (NYSE: DAY) provides cloud-based software that helps organizations manage their entire employee lifecycle, including HR, payroll, workforce management, benefits, and talent development.

Dayforce reported revenues of $464.7 million, up 9.8% year on year. This print topped analysts’ expectations by 1.5%. More broadly, it was a slower quarter as it logged revenue guidance for next quarter missing analysts’ expectations significantly.

Dayforce had the weakest full-year guidance update among its peers. The stock is up 30.6% since reporting and currently trades at $69.31.

Read our full, actionable report on Dayforce here, it’s free.

Asure Software (NASDAQ: ASUR)

Operating in the often-overlooked smaller metropolitan markets where HR expertise can be scarce, Asure Software (NASDAQ: ASUR) provides cloud-based human capital management software and services that help small and medium-sized businesses manage payroll, taxes, time tracking, and HR compliance.

Asure Software reported revenues of $30.12 million, up 7.4% year on year. This number missed analysts’ expectations by 3.2%. Overall, it was a softer quarter as it also produced EBITDA guidance for next quarter missing analysts’ expectations significantly and a significant miss of analysts’ billings estimates.

Asure Software pulled off the highest full-year guidance raise but had the weakest performance against analyst estimates and weakest performance against analyst estimates among its peers. The stock is down 13% since reporting and currently trades at $8.45.

Read our full, actionable report on Asure Software here, it’s free.

Market Update

Thanks to the Fed’s series of rate hikes in 2022 and 2023, inflation has cooled significantly from its post-pandemic highs, drawing closer to the 2% goal. This disinflation has occurred without severely impacting economic growth, suggesting the success of a soft landing. The stock market thrived in 2024, spurred by recent rate cuts (0.5% in September and 0.25% in November), and a notable surge followed Donald Trump’s presidential election win in November, propelling indices to historic highs. Nonetheless, the outlook for 2025 remains clouded by potential trade policy changes and corporate tax discussions, which could impact business confidence and growth. The path forward holds both optimism and caution as new policies take shape.

Want to invest in winners with rock-solid fundamentals? Check out our Top 6 Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.