Hilltop Holdings has had an impressive run over the past six months as its shares have beaten the S&P 500 by 8.6%. The stock now trades at $31.91, marking a 14.8% gain. This run-up might have investors contemplating their next move.

Is there a buying opportunity in Hilltop Holdings, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Do We Think Hilltop Holdings Will Underperform?

We’re happy investors have made money, but we're swiping left on Hilltop Holdings for now. Here are three reasons why we avoid HTH and a stock we'd rather own.

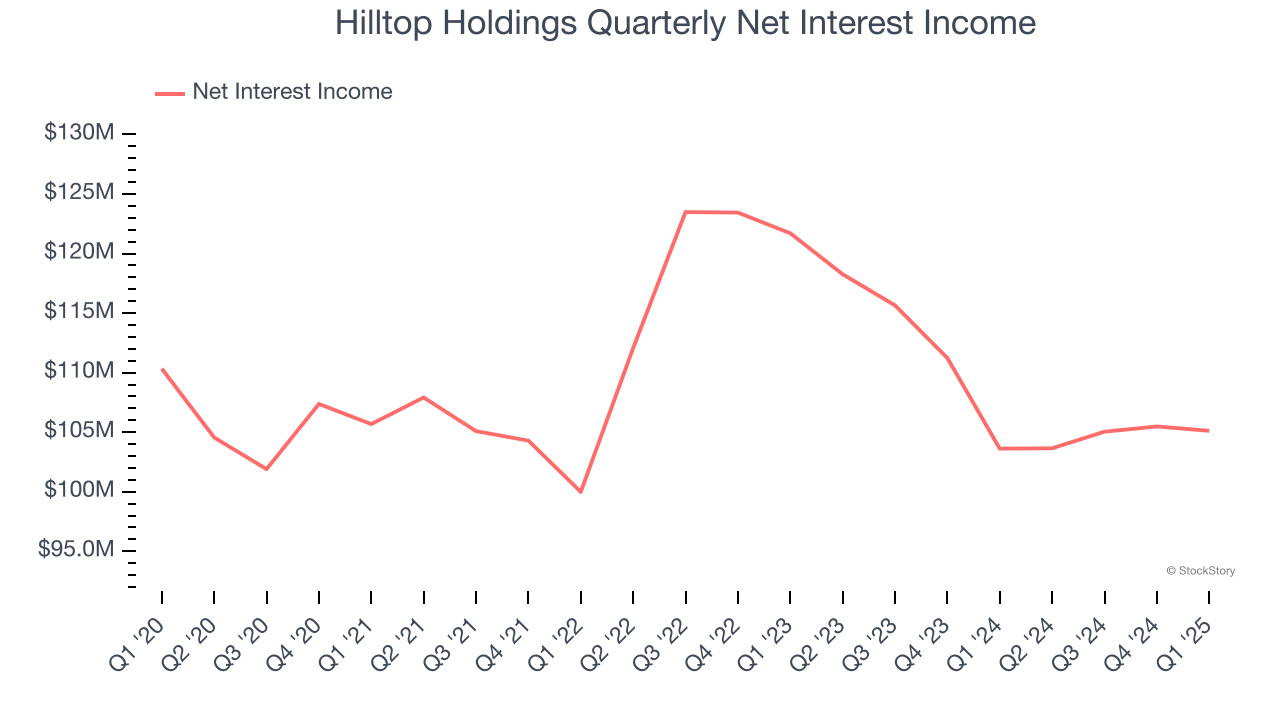

1. Net Interest Income Hits a Plateau

While banks generate revenue from multiple sources, investors view net interest income as the cornerstone - its predictable, recurring characteristics stand in sharp contrast to the volatility of non-interest income.

Hilltop Holdings’s net interest income was flat over the last four years, much worse than the broader bank industry.

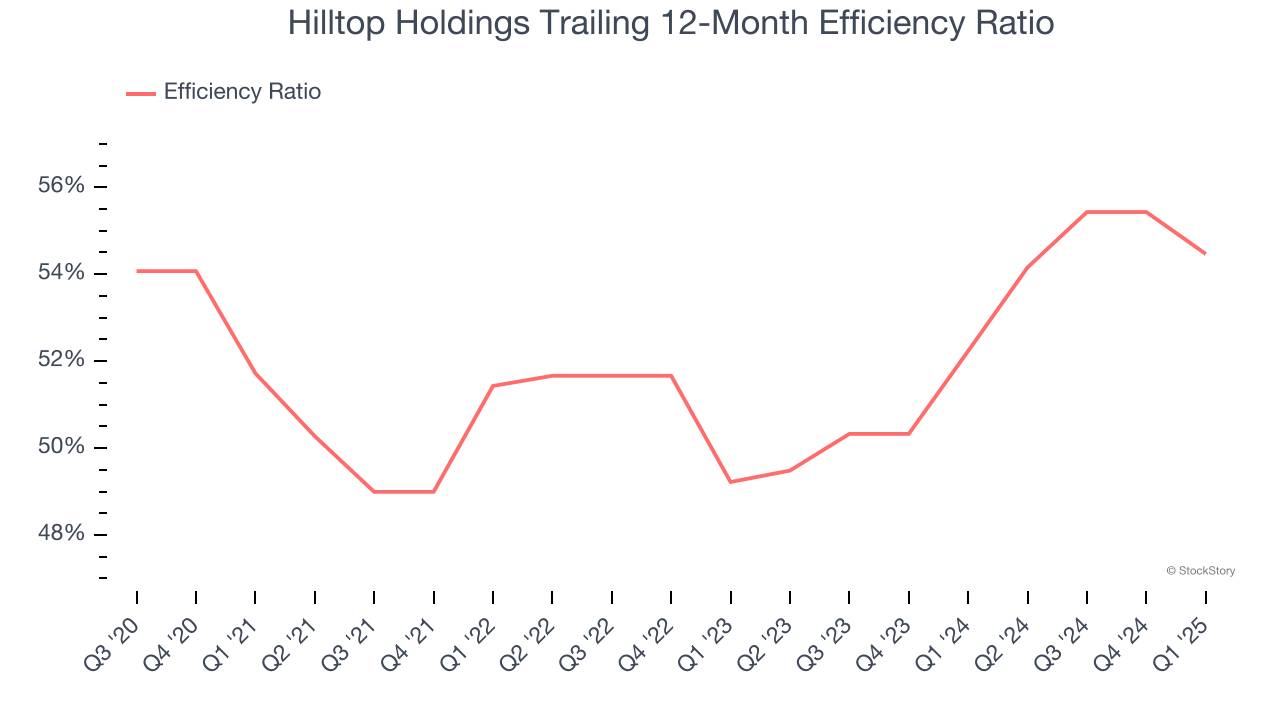

2. Efficiency Ratio Expected to Falter

The underlying profitability of top-line growth determines the actual bottom-line impact. Banking institutions measure this dynamic using the efficiency ratio, which is calculated by dividing non-interest expenses like personnel, facilities, technology, and marketing by total revenue.

Investors focus on efficiency ratio changes rather than absolute levels, understanding that expense structures vary by revenue mix. Counterintuitively, lower efficiency ratios indicate better performance since they represent lower costs relative to revenue.

For the next 12 months, Wall Street expects Hilltop Holdings to become less profitable as it anticipates an efficiency ratio of 86.5% compared to 54.5% over the past year.

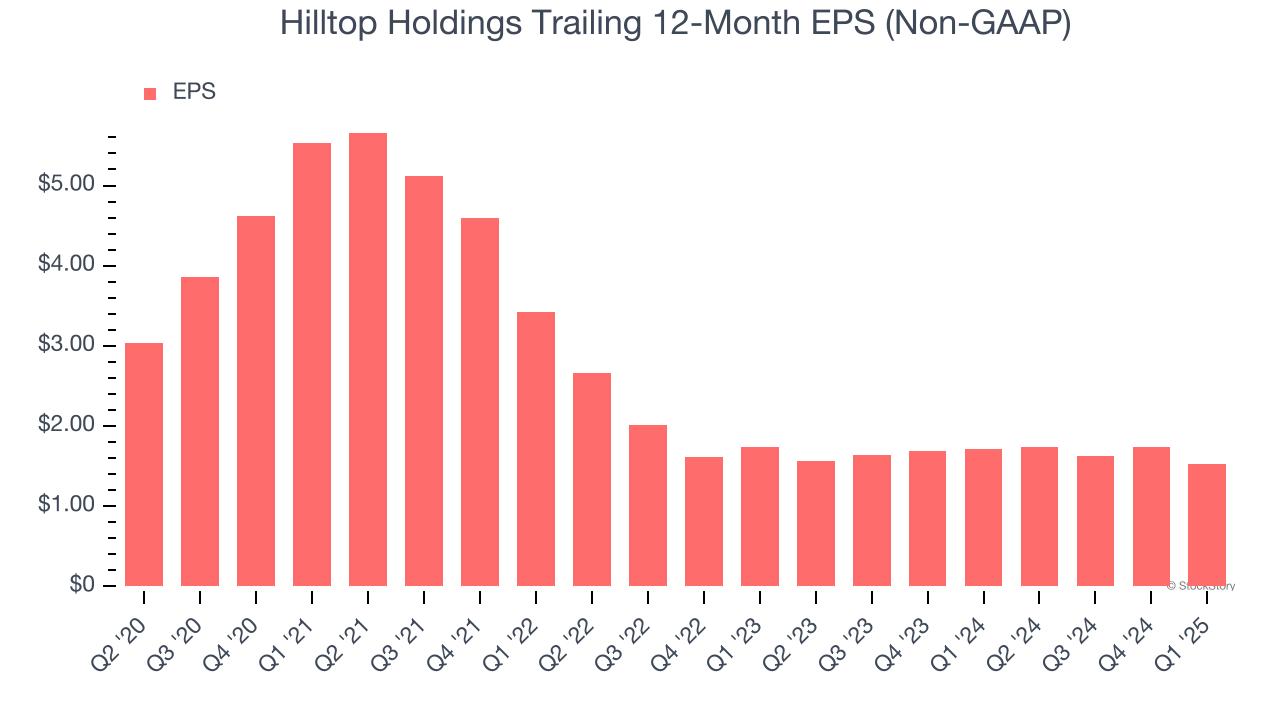

3. EPS Trending Down

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Sadly for Hilltop Holdings, its EPS declined by 9% annually over the last five years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

Final Judgment

Hilltop Holdings doesn’t pass our quality test. With its shares outperforming the market lately, the stock trades at 0.9× forward P/B (or $31.91 per share). This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think other companies feature superior fundamentals at the moment. Let us point you toward one of our top software and edge computing picks.

Stocks We Would Buy Instead of Hilltop Holdings

Market indices reached historic highs following Donald Trump’s presidential victory in November 2024, but the outlook for 2025 is clouded by new trade policies that could impact business confidence and growth.

While this has caused many investors to adopt a "fearful" wait-and-see approach, we’re leaning into our best ideas that can grow regardless of the political or macroeconomic climate. Take advantage of Mr. Market by checking out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.