Let’s dig into the relative performance of TaskUs (NASDAQ: TASK) and its peers as we unravel the now-completed Q4 business process outsourcing & consulting earnings season.

The sector stands to benefit from ongoing digital transformation, increasing corporate demand for cost efficiencies, and the growing complexity of regulatory and cybersecurity landscapes. For those that invest wisely, AI and automation capabilities could emerge as competitive advantages, enhancing process efficiencies for the companies themselves as well as their clients. On the flip side, AI could be a headwind as well as the technology could lower the barrier to entry in the space and give rise to more self-service solutions. Additional challenges in the years ahead could include wage inflation for highly skilled consultants and potential regulatory scrutiny on outsourcing practices—especially in industries like finance and healthcare where who has access to certain data matters greatly.

The 8 business process outsourcing & consulting stocks we track reported a mixed Q4. As a group, revenues beat analysts’ consensus estimates by 0.7% while next quarter’s revenue guidance was in line.

In light of this news, share prices of the companies have held steady as they are up 2.5% on average since the latest earnings results.

TaskUs (NASDAQ: TASK)

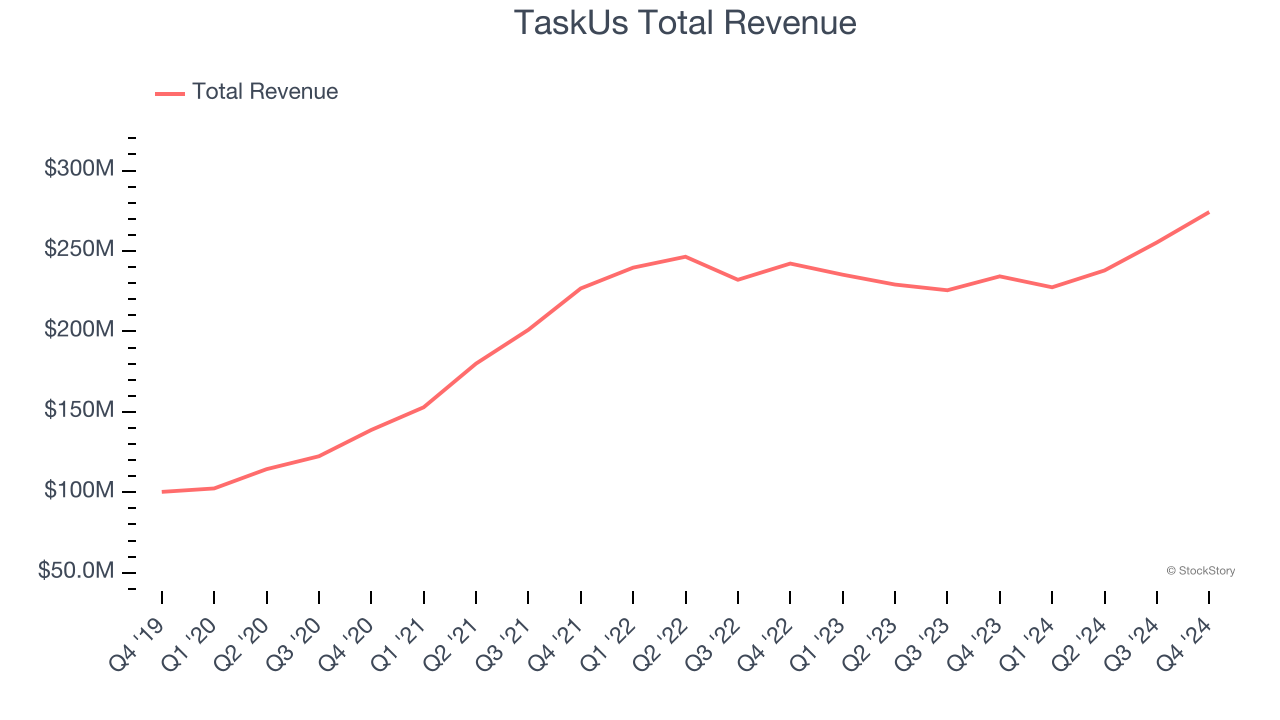

Starting as a virtual assistant service in 2008 before evolving into a global digital services provider, TaskUs (NASDAQ: TASK) provides outsourced digital services including customer experience management, content moderation, and AI data services to innovative technology companies.

TaskUs reported revenues of $274.2 million, up 17.1% year on year. This print exceeded analysts’ expectations by 2%. Despite the top-line beat, it was still a slower quarter for the company with a significant miss of analysts’ EPS estimates.

TaskUs pulled off the highest full-year guidance raise of the whole group. Unsurprisingly, the stock is up 7.2% since reporting and currently trades at $16.75.

Read our full report on TaskUs here, it’s free.

Best Q4: CRA (NASDAQ: CRAI)

Often retained for high-stakes matters with multibillion-dollar implications, CRA International (NASDAQ: CRAI) provides economic, financial, and management consulting services to corporations, law firms, and government agencies for litigation, regulatory proceedings, and business strategy.

CRA reported revenues of $181.9 million, up 5.9% year on year, outperforming analysts’ expectations by 3%. The business had a very strong quarter with a solid beat of analysts’ EPS estimates and full-year revenue guidance slightly topping analysts’ expectations.

CRA scored the biggest analyst estimates beat among its peers. The market seems happy with the results as the stock is up 21.7% since reporting. It currently trades at $196.24.

Is now the time to buy CRA? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Genpact (NYSE: G)

Originally spun off from General Electric in 2005 to provide business process services, Genpact (NYSE: G) is a global professional services firm that helps businesses transform their operations through digital technology, AI, and data analytics solutions.

Genpact reported revenues of $1.21 billion, up 7.4% year on year, in line with analysts’ expectations. It was a slower quarter as it posted revenue guidance for next quarter slightly missing analysts’ expectations.

Genpact delivered the weakest full-year guidance update in the group. As expected, the stock is down 7.3% since the results and currently trades at $45.92.

Read our full analysis of Genpact’s results here.

FTI Consulting (NYSE: FCN)

With a team of experts deployed across 30+ countries to tackle complex business challenges, FTI Consulting (NYSE: FCN) is a global business advisory firm that helps organizations manage change, mitigate risk, and resolve disputes across financial, legal, operational, and regulatory matters.

FTI Consulting reported revenues of $898.3 million, down 3.3% year on year. This number lagged analysts' expectations by 0.9%. Taking a step back, it was still a strong quarter as it put up a solid beat of analysts’ EPS estimates.

FTI Consulting had the slowest revenue growth among its peers. The stock is down 2% since reporting and currently trades at $164.89.

Read our full, actionable report on FTI Consulting here, it’s free.

Huron (NASDAQ: HURN)

Founded in 2002 during a time of significant regulatory change in corporate America, Huron Consulting Group (NASDAQ: HURN) is a professional services company that helps organizations develop growth strategies, optimize operations, and implement digital transformation solutions.

Huron reported revenues of $404.1 million, up 11.2% year on year. This result surpassed analysts’ expectations by 0.8%. It was a strong quarter as it also recorded an impressive beat of analysts’ EPS estimates and a narrow beat of analysts’ full-year EPS guidance estimates.

The stock is up 3% since reporting and currently trades at $139.98.

Read our full, actionable report on Huron here, it’s free.

Market Update

Thanks to the Fed’s rate hikes in 2022 and 2023, inflation has been on a steady path downward, easing back toward that 2% sweet spot. Fortunately (miraculously to some), all this tightening didn’t send the economy tumbling into a recession, so here we are, cautiously celebrating a soft landing. The cherry on top? Recent rate cuts (half a point in September 2024, a quarter in November) have propped up markets, especially after Trump’s November win lit a fire under major indices and sent them to all-time highs. However, there’s still plenty to ponder — tariffs, corporate tax cuts, and what 2025 might hold for the economy.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Growth Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.