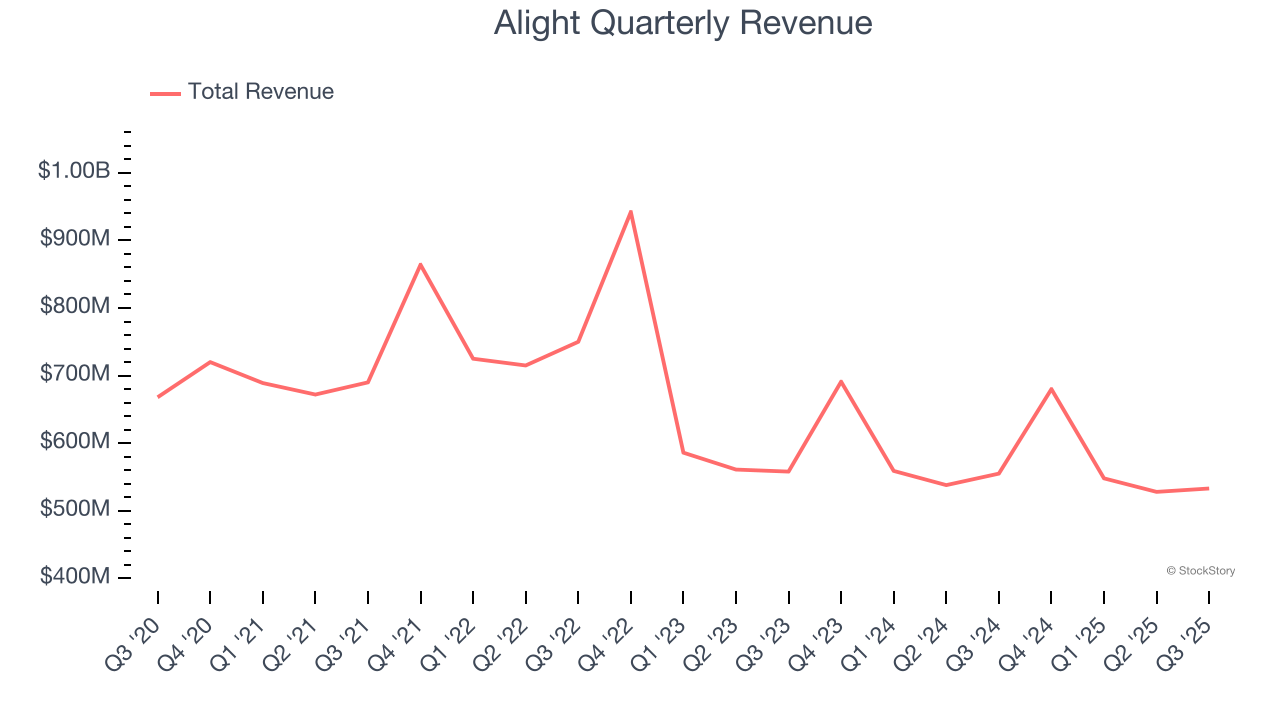

Human capital management provider Alight (NYSE: ALIT) missed Wall Street’s revenue expectations in Q3 CY2025, with sales falling 4% year on year to $533 million. The company’s full-year revenue guidance of $2.27 billion at the midpoint came in 1.6% below analysts’ estimates. Its non-GAAP profit of $0.12 per share was in line with analysts’ consensus estimates.

Is now the time to buy Alight? Find out by accessing our full research report, it’s free for active Edge members.

Alight (ALIT) Q3 CY2025 Highlights:

- Revenue: $533 million vs analyst estimates of $536.6 million (4% year-on-year decline, 0.7% miss)

- Adjusted EPS: $0.12 vs analyst estimates of $0.13 (in line)

- Adjusted EBITDA: $138 million vs analyst estimates of $136.1 million (25.9% margin, 1.4% beat)

- The company dropped its revenue guidance for the full year to $2.27 billion at the midpoint from $2.31 billion, a 1.7% decrease

- Management lowered its full-year Adjusted EPS guidance to $0.56 at the midpoint, a 8.2% decrease

- EBITDA guidance for the full year is $607.5 million at the midpoint, below analyst estimates of $624.2 million

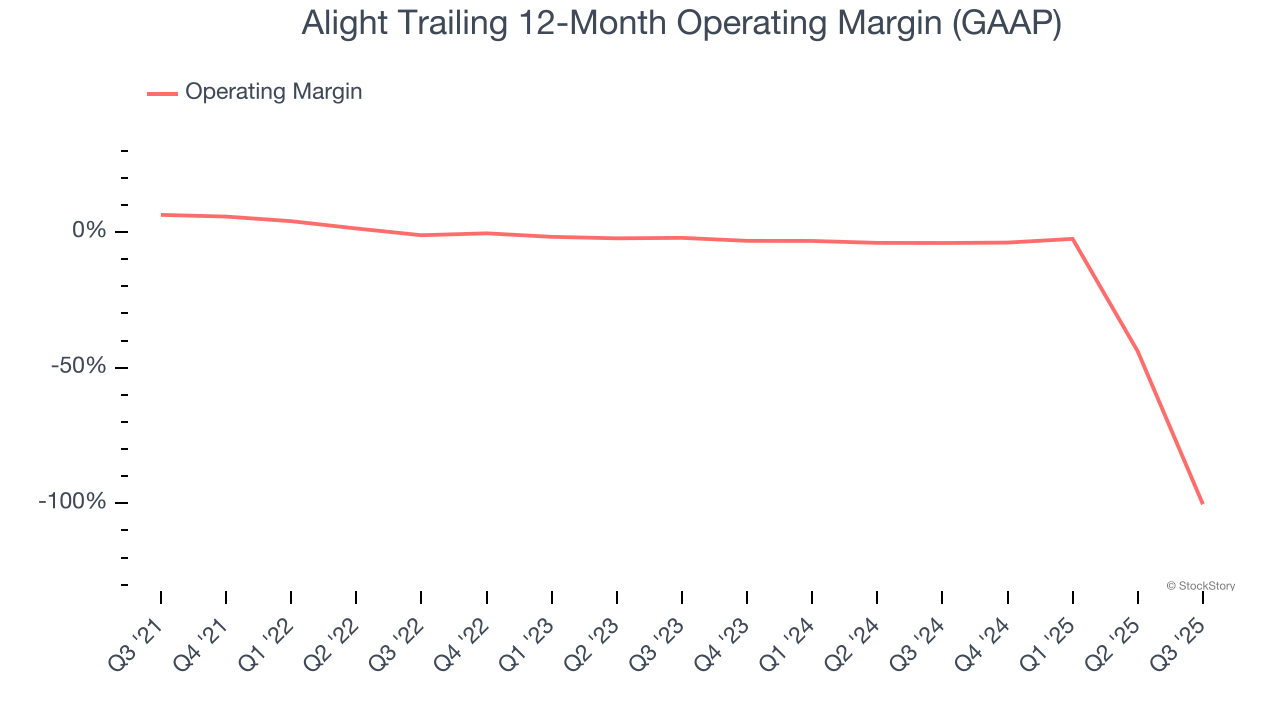

- Operating Margin: -248%, down from -7.6% in the same quarter last year

- Free Cash Flow was -$8 million compared to -$52 million in the same quarter last year

- Market Capitalization: $1.43 billion

“I am pleased with our ability to deliver enhanced outcomes for clients and their people, with participant satisfaction at record levels since the end of our technology transformation," said CEO Dave Guilmette.

Company Overview

Born from a corporate spinoff in 2017 to focus on employee experience technology, Alight (NYSE: ALIT) provides human capital management solutions that help companies administer employee benefits, payroll, and workforce management systems.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can have short-term success, but a top-tier one grows for years.

With $2.29 billion in revenue over the past 12 months, Alight is a mid-sized business services company, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale.

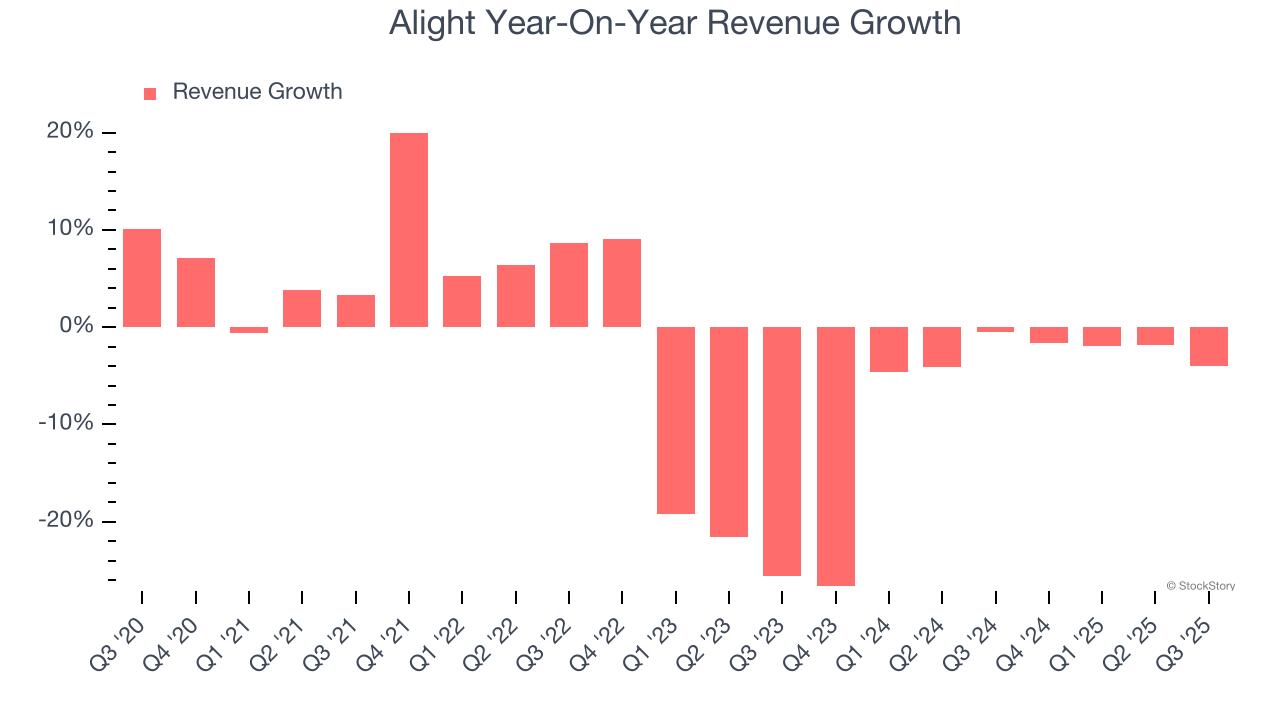

As you can see below, Alight’s demand was weak over the last five years. Its sales fell by 3.1% annually, a rough starting point for our analysis.

Long-term growth is the most important, but within business services, a half-decade historical view may miss new innovations or demand cycles. Alight’s recent performance shows its demand remained suppressed as its revenue has declined by 7% annually over the last two years.

This quarter, Alight missed Wall Street’s estimates and reported a rather uninspiring 4% year-on-year revenue decline, generating $533 million of revenue.

Looking ahead, sell-side analysts expect revenue to grow 2.1% over the next 12 months. While this projection suggests its newer products and services will catalyze better top-line performance, it is still below the sector average.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Alight’s high expenses have contributed to an average operating margin of negative 17.6% over the last five years. Unprofitable business services companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

Analyzing the trend in its profitability, Alight’s operating margin decreased significantly over the last five years. Alight’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

Alight’s operating margin was negative 248% this quarter. The company's consistent lack of profits raise a flag.

Earnings Per Share

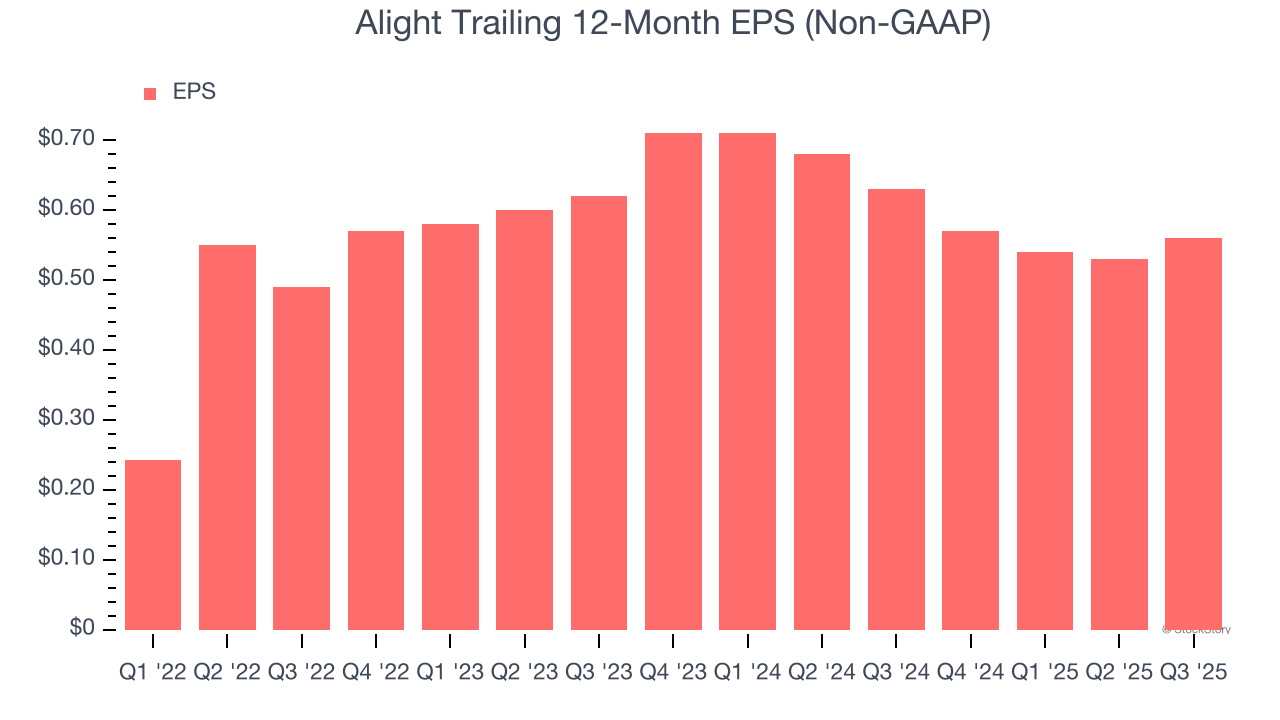

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Alight’s full-year EPS flipped from negative to positive over the last four years. This is encouraging and shows it’s at a critical moment in its life.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

Sadly for Alight, its EPS and revenue declined by 5% and 7% annually over the last two years. We tend to steer our readers away from companies with falling revenue and EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, Alight’s low margin of safety could leave its stock price susceptible to large downswings.

In Q3, Alight reported adjusted EPS of $0.12, up from $0.09 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates, but we care more about long-term adjusted EPS growth than short-term movements. Over the next 12 months, Wall Street expects Alight’s full-year EPS of $0.56 to grow 12%.

Key Takeaways from Alight’s Q3 Results

We struggled to find many positives in these results. Its full-year EPS guidance missed and its EPS was in line with Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 2.8% to $2.62 immediately after reporting.

Alight didn’t show it’s best hand this quarter, but does that create an opportunity to buy the stock right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.