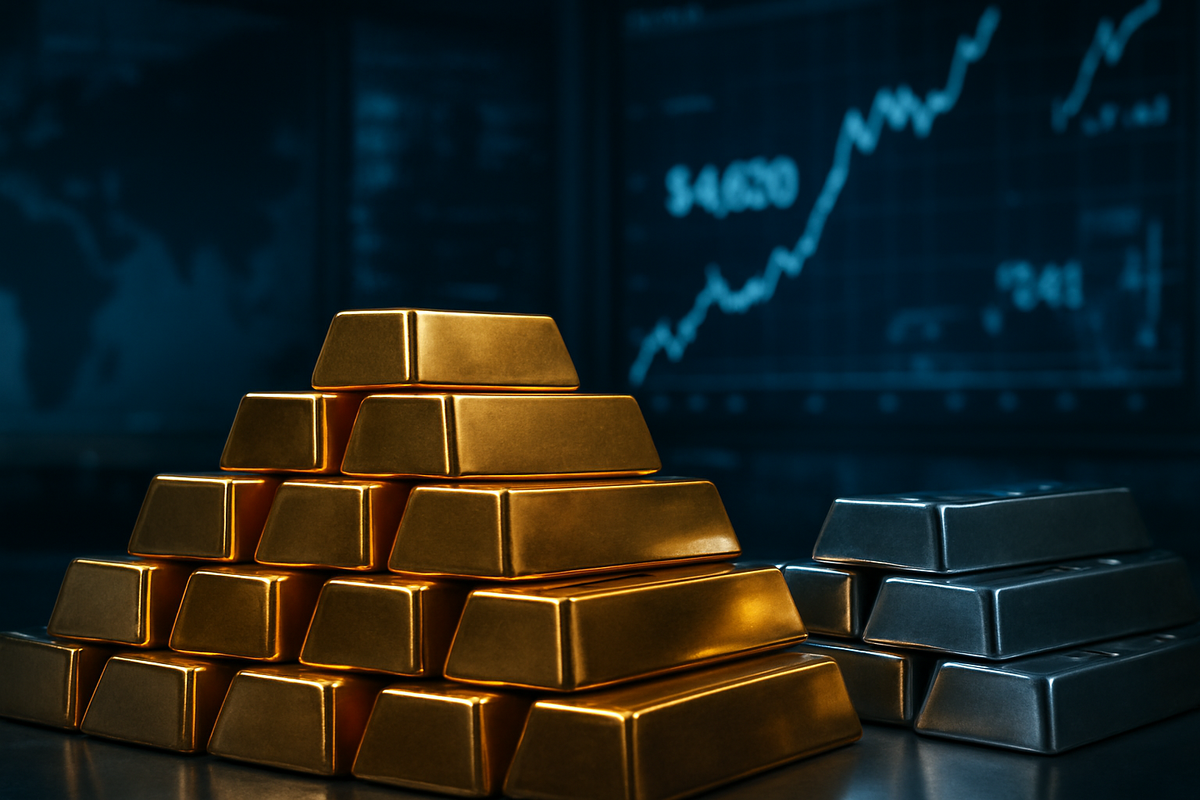

As of January 13, 2026, the global financial landscape has been fundamentally reshaped by a historic surge in precious metals. Gold has shattered expectations, climbing to an unprecedented $4,630 per ounce, while silver has staged a parabolic run to reach $84 per ounce. This dual rally, which began in earnest during the final quarter of 2025, represents a seismic shift in investor sentiment as the traditional "safe-haven" trade transforms into a mandatory hedge against systemic risk. The immediate implications are profound: a massive transfer of wealth into hard assets, a direct challenge to the supremacy of the U.S. dollar, and a scramble by industrial manufacturers to secure dwindling silver supplies.

The current price action is not merely a speculative bubble but the culmination of a "perfect storm" of geopolitical and monetary triggers. The rally intensified on January 1, 2026, when China implemented strict two-year licensing requirements for silver exports, effectively choking off 60% of the global supply for a metal critical to the green energy transition. This was compounded by a domestic crisis in the United States, where reports of a "Fed Independence Crisis" emerged. Market volatility spiked following rumors that the executive branch had threatened Federal Reserve Chair Jerome Powell with legal action, raising existential questions about the politicization of U.S. monetary policy.

A Timeline of Turbulence and Accumulation

The path to $4,600 gold was paved by three years of relentless central bank accumulation. In 2024, net purchases by central banks exceeded 1,000 tonnes for the third consecutive year, led by nations such as Poland, Turkey, and Uzbekistan. By 2025, this trend evolved from opportunistic buying to a structural "de-dollarization" strategy. Estimates suggest that "shadow" buying—unrecorded purchases by major Eastern economies—pushed the 2025 total closer to 850 tonnes, as nations sought to insulate their reserves from U.S. sanctions and currency fluctuations.

The initial market reaction in early January 2026 has been one of controlled panic among institutional shorts. As gold breached the psychological $4,500 barrier, a massive short-covering rally ensued, further propelling prices. Major investment banks, including Goldman Sachs and JP Morgan, have been forced to revise their year-end targets upward, with some now calling for $5,000 gold by the fourth quarter of 2026. The geopolitical risk premium has been further inflated by a military blockade in Venezuela and escalating tensions in Iran, which have kept energy and metal markets in a state of high alert.

Winners and Losers in the New Metal Economy

The primary beneficiaries of this historic run are the major mining conglomerates, which are currently enjoying record-breaking free cash flow. Newmont Corporation (NYSE: NEM), the world’s largest gold producer, saw its stock hit an all-time high of $106 this week, bolstered by a production forecast of 5.6 million ounces for the year. Similarly, Barrick Gold (NYSE: GOLD) has emerged as a top performer, with its shares surging over 180% since the start of 2025. The company’s focus on "Tier One" assets and the successful restart of its Loulo-Gounkoto operations in Mali have made it a favorite among institutional investors.

In the silver space, Wheaton Precious Metals (NYSE: WPM) has capitalized on its "streaming" model, maintaining a staggering 77% net profit margin as silver prices nearly tripled in eighteen months. Agnico Eagle Mines (NYSE: AEM) and mid-tier producer Alamos Gold (NYSE: AGI) have also outperformed the broader markets, with AEM remaining a staple for dividend-seeking investors. However, the news is not positive for everyone. Industrial giants in the solar and electric vehicle (EV) sectors are facing a "silver squeeze." Companies like Tesla (NASDAQ: TSLA) and major solar panel manufacturers are seeing their margins eroded by the soaring cost of silver paste, leading to concerns that the green energy transition could stall due to raw material unaffordability.

The Wider Significance: A Multipolar Reserve System

The ascent of gold and silver in 2026 marks a turning point in the history of global finance. It signals a move away from a unipolar, dollar-centric world toward a multipolar reserve system where hard assets play a central role. This trend fits into a broader industry shift where "real assets"—commodities, land, and precious metals—are outperforming paper assets for the first time in decades. The regulatory implications are significant; we are seeing a push for new transparency laws regarding central bank holdings and a potential re-evaluation of how gold is weighted in international banking capital requirements (Basel III/IV).

Historically, this rally draws comparisons to the late 1970s, yet the current environment is unique due to the industrial demand for silver. Unlike the 1980 peak, which was purely inflationary, the 2026 peak is driven by a structural supply deficit that has persisted for five years. The "ripple effect" is already being felt by competitors in the mining industry, as junior explorers and development-stage companies see a massive influx of venture capital, potentially leading to a new era of consolidation and M&A activity as majors look to replace their depleting reserves.

What Comes Next: $5,000 Gold and Beyond?

In the short term, analysts expect a period of consolidation as the market digests the rapid gains of early January. However, the long-term outlook remains bullish. If the "Fed Independence Crisis" is not resolved, or if China maintains its silver export ban, the potential for $5,000 gold and $100 silver becomes a baseline scenario rather than a "moonshot" prediction. Strategic pivots are already underway; many industrial users are aggressively researching silver-free alternatives for photovoltaic cells, though such technology is likely years away from commercial viability.

Market participants must also prepare for increased volatility. While the trend is upward, the "geopolitical risk premium" is notoriously fickle. Any de-escalation in the Middle East or a surprise stabilization of U.S. fiscal policy could trigger a sharp, albeit likely temporary, correction. The challenge for investors will be distinguishing between a healthy pullback and a fundamental change in the macro environment.

Summary and Investor Outlook

The historic peaks reached by gold and silver in January 2026 represent more than just a price milestone; they are a barometer of global instability and a loss of faith in traditional fiat currencies. Central banks have led the way, proving that in an era of geopolitical strife, gold remains the ultimate neutral reserve asset. For the market moving forward, the focus will shift from "if" prices will rise to "how high" they can go before industrial demand is permanently destroyed.

Investors should closely watch the Federal Reserve’s autonomy and any further trade restrictions from the East. The performance of miners like Newmont and Barrick Gold will serve as a bellwether for the sector's health. While the "Golden Age of 2026" offers immense opportunities, it also serves as a stark reminder of the fragility of the modern financial system. The coming months will determine whether these record prices are the new floor or a temporary ceiling in a rapidly changing world.

This content is intended for informational purposes only and is not financial advice