Whether early in your working career, halfway through or nearing retirement, it pays to have an individual retirement account (IRA). IRAs are a familiar financial instrument, but there are always people new to IRAs. This article will help you better understand IRAs and how to invest in an IRA in seven simple steps.

Overview of an Individual Retirement Account (IRA)

IRAs were created in 1974 by the U.S. Congress as part of the Employee Retirement Income Security Act (ERSA). Congress created the Act to protect workers’ retirement income, regulate pension plans, and encourage individuals to save for retirement. IRAs paved the way for individuals and workers who didn’t have access to retirement pensions or 401(k) plans offered by their employers. It was an opportunity for them to partake in a tax-advantaged plan that enables them to personally make tax-deductible contributions with tax-deferred benefits as investments grow in value, taking advantage of the compounding effect over time.

IRAs have since evolved into a popular and widely used retirement savings vehicle for ages and all people, including those who may already have an employer-sponsored retirement plan. Keep in mind that the Internal Revenue Service (IRS) uses the term individual retirement arrangement (IRA), which is synonymous and interchangeable with individual retirement accounts (IRAs). There are several types of IRA plans, which we will review in this IRA guide as we review how to start an IRA.

How to Open an IRA

Here are the seven simple steps to follow when getting started with IRAs.

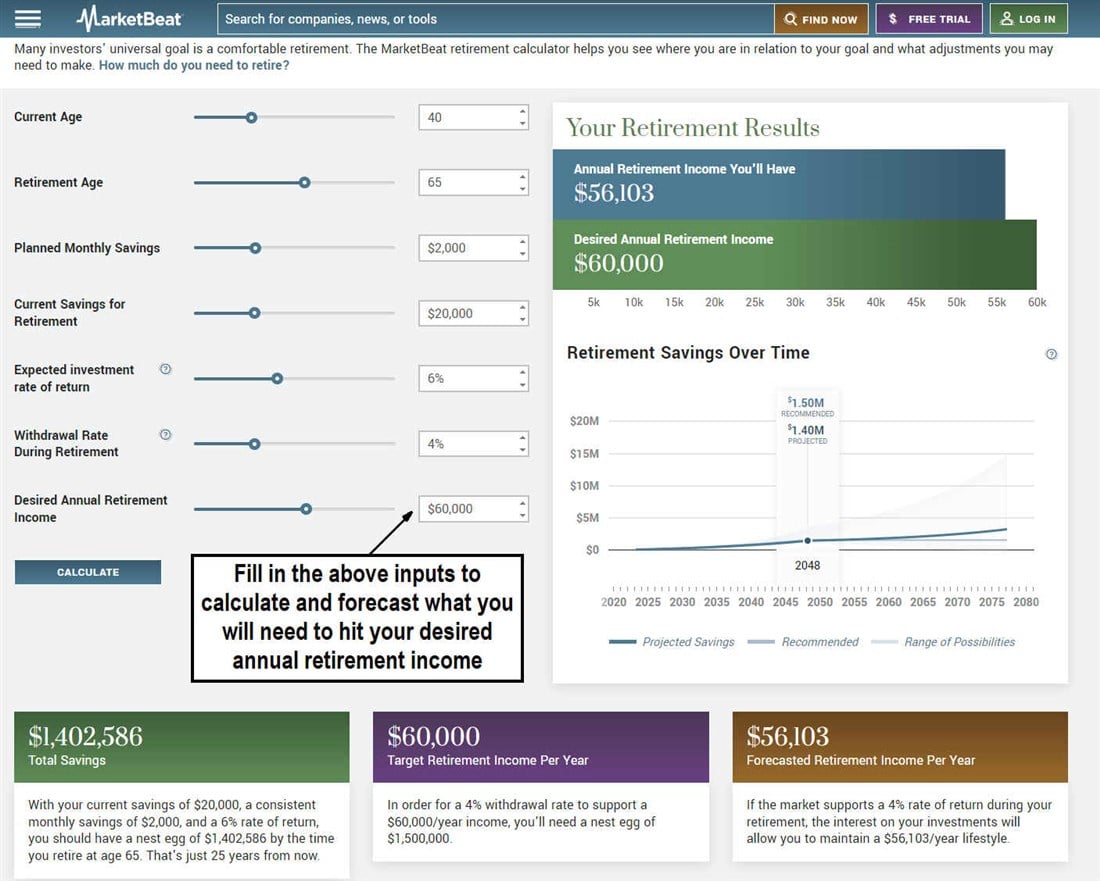

Step 1: Calculate your desired annual retirement income.

Before you learn how to invest in an IRA account, consider your desired annual retirement income first. MarketBeat’s retirement calculator can help you calculate what factors can help you reach your goal for how to invest in IRA.

By accurately filling in the required inputs from “current age” through “desired annual retirement income,” the retirement calculator shows you a range of possibilities identifying what adjustments will be needed to reach your desired retirement income.

It will calculate total savings and forecasted retirement income per year and suggest what kind of nest egg you would need to hit your target annual retirement income. You will notice that the lower your current age, the more your savings grow over time.

Step 2: Select a financial institution or provider for your IRA.

An IRA is a tax-advantaged savings account. It has to be opened at a financial institution, including at licensed stock brokerage firms, chartered banks, credit unions, robo-advisors, mutual fund companies or online brokers. Each type of institution will have fees, account platforms and features, investment options and customer service.

Stock brokerages have the most options for picking the various investments in your IRA. They provide access to many investments, including stocks, mutual funds, exchange-traded funds (ETFs), bonds and other securities of all risk levels. Banks tend to be more conservative and limited to certificates of deposit (CDs), savings accounts and a limited number of mutual funds. Contact and compare which institution(s) you feel comfortable with since it can be a long-term commitment. You may want to call customer service and ask questions like, “What is an IRA account and how does it work?” These questions can give you an idea of how knowledgeable and supportive its representatives are.

Once you’ve decided where to open an IRA, go ahead and complete the application online and carefully read how to start an IRA account. When setting up an IRA, the application will ask many personal questions, including your Social Security number, date of birth, employment and income and beneficiaries. If you feel more comfortable working through this information in-person, consider setting up an appointment at a local branch office, if available.

Step 3: Choose your account type.

There are several types of IRAs to select from when opening an account. Here are three main types of IRAs to select from:

- Traditional IRAs: This is the original IRA plan created by Congress in 1974. It enables individuals without employer retirement plan coverage to make tax-deductible contributions to their IRA accounts. If you or your spouse is covered under an employer-sponsored retirement plan, then your tax deduction will be limited based on your income. There are annual contribution limits that can be made depending on your age. For example, in 2023, the annual maximum IRA contribution limit is $6,500 if you're under 50 and $7,500 if you're 50 or older. The IRS sets current annual contribution limits. Taxes on capital gains are deferred until funds are withdrawn at retirement or after 59 ½ years of age. This means investment profits are taxed once the investment is cashed out and withdrawn from the IRA in retirement. The capital gains (profits) are taxed at the ordinary income tax rate, not the long-term capital gains tax rate. If you make IRA withdrawals before turning 59 ½ years old, you will receive a 10% penalty in addition to having to claim proceeds as gross income, which also gets taxed accordingly.

- Roth IRAs: For those individuals who don’t want to be burdened with paying taxes on withdrawals, Roth IRA contributions are made with after-tax dollars. Since income taxes are already paid, qualified withdrawals are tax-free after 59 ½ years old, provided you've had the Roth IRA account for at least five years. Withdrawals before age 59 ½ are subject to a 10% penalty and taxed as ordinary income. There are a few exceptions that can bypass the penalty, but the proceeds are still taxed as ordinary income. These exceptions can range from first-time home purchases to qualified educational, birth, disability, and medical expenses. It's best to double-check with your financial institution if the need for early withdrawal arises. Here’s a Roth IRA calculator on MarketBeat to see how growth can change based on different inputs. Here is a way to determine if a Roth IRA is right for you.

- SEP IRAs: Simplified employee pension (SEP) IRAs are designed for small business owners, self-employed individuals, and employees. Contributions to a SEP IRA are made directly by the employer only. Employees can't make contributions. Contributions are tax-deductible for the business, which creates an incentive to help lower its taxable income. Like a traditional IRA, the earnings are tax-deferred and paid as ordinary income upon withdrawal during retirement. SEP IRA annual contributions tend to have higher limits than traditional IRAs. Employers can decide if, how much and when to contribute to the SEP IRA each year. SEP IRAs are a worthy retirement plan option for self-employed individuals due to the higher contribution limits and tax benefits. Withdrawal rules and penalties are the same as traditional IRAs.

Step 4: Fund your IRA account.

Once you’ve opened the IRA account, it needs to be initially funded before you can select your investments. The initial contribution can be transferred from your bank or brokerage. There are options to wire transfer, use electronic funds transfer (EFT) transfer and deposit or mail in a check. Mailing in a check takes the longest since it has to arrive at the provider, and the deposit needs time to clear in many cases before funds are available.

Roth IRA contribution eligibility requirements and tax deduction limits for traditional IRAs are based on your modified annual gross income (MAGI). MAGI is calculated by adding certain deductions to your adjusted gross income (AGI). The following deductions and exclusions are added back to your AGI to derive your MAGI:

- Traditional IRA deduction

- Student loan interest deduction

- Exclusion of employer-provided adoption benefits

- Exclusion of qualified savings bond interest

- Foreign housing deduction

- Foreign earned income exclusion

Step 5: Select your investments.

IRA investing can be a tricky endeavor. IRAs allow for investments in stocks, bonds, mutual funds, ETFs, annuities and unit investment trusts (UIT). It can be tempting to chase entries on momentum stocks but avoid the temptation. A conservative approach should be taken when you start. Index mutual funds and ETFs leave the stock picking and management in the hands of professionals. You can also invest in themes, sectors and industries through ETFs and mutual funds.

Here’s an overview of stock market sectors to review and top-rated stocks to buy if looking for ideas. Fixed-income instruments like treasury bonds can be used to balance the volatility in your IRA portfolio. Selecting individual stocks is risky and should only be considered after consulting with a registered investment advisor.

These are long-term investments, so be prudent to research and stay on top of any individual stocks if you add them. Keeping a balanced portfolio of different financial assets is prudent for controlling your risk exposure. Feel free to consult with professionals if you have specific questions on how to invest in an IRA account.

Step 6: Make regular contributions.

If you’re wondering how many IRAs you can have, the answer is as many as you want. However, annual contribution limits apply to the combined total of all your IRA accounts. It’s beneficial to make regular contributions to your IRA account. Many people only make contributions near the end of the year in a lump sum, which can get them in at disadvantageous prices. By making regular contributions, you can better dollar-cost average your investments to attain better prices.

Here’s a quick snapshot of the different types of IRAs and their tax filing status, MAGI limits and contribution limits for each.

|

IRA Type |

Tax Status |

MAGI Limits for Deductions |

Contribution Limits |

|

Traditional IRA |

Contributions may be tax deductible and withdrawals are taxed as ordinary income |

Deductibility phases out based on participation in an employer sponsored retirement plan and MAGI. If filing single and MAGI under $73,000 or married and MAGI under $116,000 then can take full tax deduction up to contribution limit. |

For 2023: $6,500 limit and $7,500 if aged 50 or older |

|

Roth IRA |

Contributions are not tax deductible and withdrawals are tax-free |

Phase-out ranges on tax filing status |

For 2023: $6,500 limit and $7,500 if aged 50 or older |

|

SEP IRA |

Contributions are tax deductible and withdrawals are taxes as ordinary income |

No MAGI limits since contributions can only be made by the employer |

Up to 25% of employee’s compensation or $66,000 for 2023 |

Step 7: Review your IRA investments periodically.

While IRAs are long-term investments, check on how the individual investments within the IRA are performing against the current market landscape and benchmark indexes like the S&P 500 index. While it's not a good idea to watch every position constantly, it is prudent to keep track of performance quarterly or semi-annually. IRAs shouldn't be used for day trading. They are a long-term commitment, but sometimes IRAs may need some portfolio rebalancing. This may require the assistance of a professional advisor to get recommendations and better spread out the risk while optimizing returns.

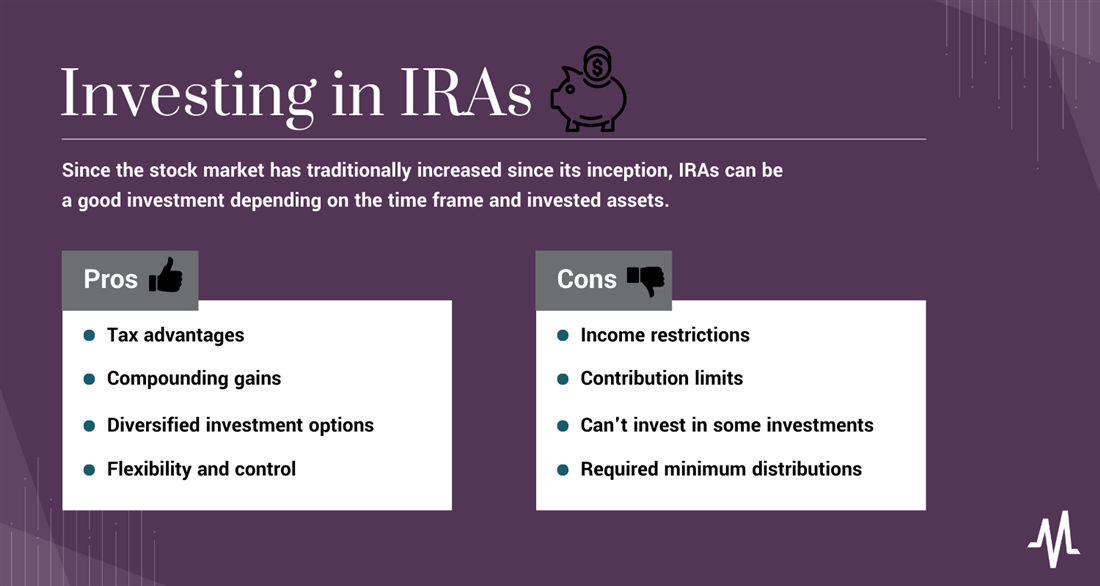

Pros and Cons of Investing in IRAs

IRA investing has its pros and cons. It's up to you to weigh them and decide if the pros outweigh the cons before investing in IRAs.

Pros

There are many advantages to investing in IRAs. Here are some key pros:

- Tax advantages: Traditional IRAs enable tax-deferred growth for your investments, which means you pay income taxes on withdrawals. Roth IRAs are paid with after-tax funds, so you won't be taxed capital gains on your investments.

- Compounding gains: IRAs enable you to compound your gains over time. Since capital gains are paid throughout the life of the IRA, those potential taxes would help grow your gains.

- Diversified investment options: IRAs allow you to invest in various financial asset classes. This also depends on your IRA provider, as stock brokerages tend to offer more investment options than banks.

- Flexibility and control: You are in charge of making your investment contributions and decisions. You don't have to depend on an employer to decide whether to or how much to contribute to your retirement plan or wait for it to vest.

Cons

It’s not all roses all the time. There are cons involved with invest IRA as well. Some of the cons include the following:

- Income restrictions: IRAs come with restrictions based on your income levels to determine eligibility and tax deduction limits. High-income earnings may not be able to tax deductions on traditional IRA contributions. High-wage earners may even be unable to contribute directly to a Roth IRA.

- Contribution limits: There is an annual limit to the amount you can contribute to an IRA. Unlike FDIC insurance, having multiple IRAs don't matter since contribution limits apply to the cumulative total of all IRA accounts.

- Cannot invest in some investments: Certain assets are not allowed in IRAs. These include life insurance, collectibles and most coins, personal real estate, derivatives, short selling, or the use of margin.

- Penalties and fees: Taking unqualified withdrawals from an IRA before turning 59.5 years of age will result in penalties. The penalties can be costly at 10%. Fees can vary depending on the IRA provider.

- Required minimum distributions: Traditional IRAs must start taking required minimum distributions starting at the age of 72. This may be different from your desired distribution plans. Roth IRAs do not have that requirement.

FAQs

Here are answers to frequently asked questions about IRAs and how to set up an IRA.

How much money do you need to start an IRA?

IRAs technically don't have minimum investment requirements. However, some providers may have their minimums to open an IRA account. Keep in mind that many mutual funds also have required minimum investments which could range from $500 and higher. Be sure to check with the financial institution on the minimums and any additional fees associated with having an IRA account.

How do you make money with an IRA?

You make money in an IRA by selecting the suitable financial instruments and holding them until retirement. The compounding effect tends to amplify investment returns in a balanced portfolio. Be careful not to day trade or take short-term speculations in an IRA.

Can I open an IRA on my own?

IRAs must be opened with licensed providers like banks, brokers or credit unions. You can open an IRA individually with any licensed provider. You can't just create an IRA account out of thin air.

You may also wonder, “How many IRAs can you have?” The IRS sets no limits on the number of IRAs you can own.

Are IRAs a good investment?

Since the stock market has traditionally increased since its inception, IRAs can be a good investment depending on the time frame and invested assets. Picking individual stocks in an IRA can be risky, especially if the company goes out of business or has years of underperformance. Investing in benchmark indexes through mutual funds or ETFs is a suitable investment over a long-term horizon. Before you dive in, learn everything you can about how to open an IRA account.